Offshore Banking:

Where and How to Open the BEST Offshore Bank Account for Your Needs

-

AUTHOR

James Hickman -

LAST UPDATED

February 8, 2022

What's the most important thing you need to know if you're considering offshore banking?

It’s that not all offshore bank accounts are created equal…

The number one mistake we see people making is that they focus only on the “offshore” part and end up with a bank account that is even riskier and even less private than their domestic one…

That’s why in this in-depth article you’ll not only learn where and how to open an offshore bank account in 2020, but also how to ensure it’s the BEST account for your PERSONAL situation.

And since everyone has a different definition of what’s best for them, we break the options down for safety, ease of opening, competitive interest rates and high net worth banking.

In this In-Depth Article

Want To Get Started Right Away?

Then download the free preview of our Ultimate Offshore Banking Guide & Comparison to get even more actionable information.

The information in this Offshore Banking Report is from before COVID-19.

We’ll be updating the guide once the new numbers are in.

In this section you’ll learn the three top reasons to open an offshore bank account… and the one important reason NOT to.

On Friday, March 15, 2013, people across the entire nation of Cyprus went to bed, with no concern about their banking system.

The next morning, suddenly, all bank accounts in the country were frozen. ATM withdrawals were limited to only 100 euros per day.

Cyprus’ banking system was totally broke. The government proclaimed a ‘bank holiday’, and banks remained closed for the next several days.

Eventually, a plan materialized: substantial portions of deposits over 100,000 euros would be confiscated in exchange for equity in the banks.

(Just imagine – Bank of America, RBC, or Lloyds takes your money and gives you stock certificates that subsequently plummet in value!)

And for everyone else, severe capital controls were instituted – some of the worst in decades.

But not everyone was restricted to the 100 euro limit…

One of Sovereign Man’s readers was living in Cyprus at the time.

He was able to continue withdrawing as much as he needed from his offshore bank account while everyone else was struggling to pay their bills.

This woman was unfortunately not prepared…

Do you think it’s far-fetched that your bank could collapse? Think again...

Few people ever give much thought to the safety and security of their bank

And why should they? After all, banks go out of their way to instill an overwhelming sense of confidence that they’re rock solid.

They spend spectacular amounts of money on ornate lobbies in giant buildings with marbled floors and buy the naming rights to football stadiums.

The unfortunate reality, however, is that many banks in the United States, Europe and the rest of the world are in a precarious condition.

In 2008, the world learned the hard way that even western banks aren’t as safe as they want us to believe.

Suddenly, OVERNIGHT, some of the largest banks in the world collapsed: Wachovia. Lehman Brothers. Washington Mutual. Dozens of banks vanished — in an instant.

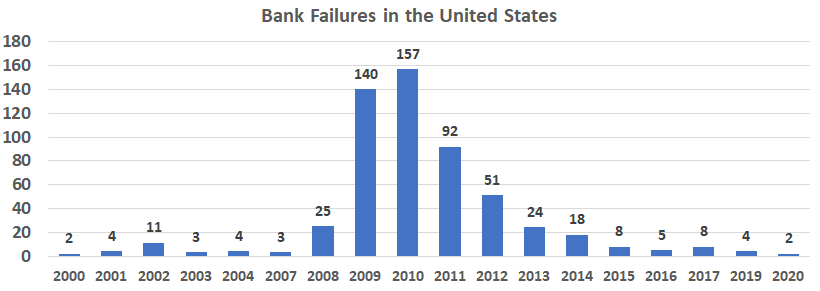

And more banks continued to fold. From 2008 to 2012 the Federal Deposit Insurance Corporation (FDIC) had to bail out 465 different banks in the United States.

The unfortunate truth is that banks regularly fail even in good times…

Bank Failures in the United States since 2000

In 2019, four US banks had to be bailed out. The economy was slowing, but still much stronger than 2020, and unemployment was at a record low.

Still, four banks went bust.

During good times, that’s not a big problem, because depositors are protected by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 in deposits.

But while they can bail out a few failing banks here and there…

The FDIC is hopelessly underfunded to handle a large-scale banking crisis

The FDIC is supposed to be the backstop for the banking system.

And for this purpose, the FDIC has some reserves – $110 billion, to be exact.

But the entire US banking system is $13 TRILLION.

That $110 billion covers less than 1% of the US banking system! During normal times (when the economy is performing, unemployment is low and steady, banks are not collapsing, etc.), the FDIC’s woefully undercapitalized capital is still generally sufficient.

But, as you know, these are far from normal times.

There are countless unemployed individuals, millions of shuttered small businesses, and bankrupt big companies collectively owe the banks trillions of dollars.

You probably know that old saying – if you owe the bank a million dollars and can’t pay, you have a problem. If you owe the bank a billion dollars and can’t pay, the bank has a problem.

That’s what we’re seeing now.

Businesses and individuals cannot pay their creditors… which means the entire banking system has a problem.

And the problem may become much worse… What if there is no economic recovery? What if a double-digit unemployment rate is the new normal? Total loan losses could easily be in the trillions of dollars.

And across most of the western world, conditions are about the same.

In Canada, for example, the Canadian Deposit Insurance Corporation insured C$807 billion in deposits in 2019. But they only have a reserve of only C$5.0 billion – or just six-tenths of one percent. Canada’s May 2020 unemployment rate was 13.7%, and like the US, individuals and businesses are suffering.

And the economic consequences of COVID-19 make it even more important to consider the safety of your bank

Now, more than ever, is the time to be concerned about your savings held at banks.

When COVID-19 first broke out in the United States, the FDIC felt the need to publish a bizarre video saying…

Your money is safe at the banks. The last thing you should be doing is pulling your money out of the banks thinking it’s going to be safer somewhere else.

– Jelena McWilliams, FDIC Chairman

To the curious observer, this raises an interesting point: why is the FDIC asking us to NOT withdraw our savings?

If the financial system is so safe, it shouldn’t matter to them whether or not people keep their money in the banks.

Yet they still felt the need to specifically ask people to NOT withdraw their money… and tell us that we shouldn’t keep cash at home.

The FDIC also insists that they’ve always been able to prevent depositors from losing money. “Not a single depositor has lost money since 1933.” And that’s true.

But they’ve never had to deal with this before. Neither the FDIC, nor any bank, has ever had to deal with a complete shutdown of the economy… or potential losses of this magnitude.

The Covid-19 impact on the banking system could be 10x bigger than the housing meltdown in 2008 and right now, it’s simply too early to tell what the final impact will be.

Global debt is a staggering $250 TRILLION and the banks are ultimately on the hook

$250 TRILLION of global debt…

That’s more than 176% of global Gross Domestic Product (GDP), or the entire economic output of every single country in the world.

And the debt will surely be a larger problem for banks…

Earlier this year, US unemployment jumped to 14.7% – the worst since the Great Depression. Thousands of businesses are failing. Payments for over 7% of active US mortgages are delayed.

It’s a similar story all across the world.

Businesses are unable to pay back loans. Individuals cannot pay mortgages, credit cards and other debt.

Ultimately, the banks are on the hook for all of this.

Again, there’s $250 trillion in global debt right now.

But total bank capital worldwide is less than $10 trillion. So if individuals and businesses that have been affected by COVID-19 default on just 4% of the total debt, it will wipe out ALL of the world’s banking capital.

This means that in a crisis, YOUR money on deposit at banks might be compromised.

And worst of all… there’s ZERO transparency and we won’t know the depth of the banking crisis until it’s too late...

One of the most important things you need to understand is that the moment you deposit your savings at a bank, it’s no longer your money.

From a legal perspective, your savings become the bank’s money; as a depositor, you have nothing more than an unsecured claim against the bank.

And most banks in the western world are no longer conservative, responsible financial stewards.

Instead they view their clients as cash-cows whose money they can use to gamble on the latest investment fad, no matter how stupid and destructive it might be.

They give ‘no money down’ loans to homeless people with no employment history and risk their depositor’s savings on destructive and complicated financial instruments like derivatives.

That’s exactly what almost brought down the entire financial system in 2008.

After a short period of deleveraging, US banks acted as if nothing had happened. They picked up right where they left off and now hold a record amount of derivative instruments

And whether in Europe or the US, there is close to zero transparency in the banking system. No one knows what’s really going on behind the scenes. A bank’s balance sheet cannot reveal which loans are sound and which loans will soon be in default.

Fortunately, there are still banks around the world that are responsible, conservative stewards of their client’s finances...

Some banking systems have much stricter and safer criteria than banks in the west.

A word of caution, though, upfront: These numbers are from before COVID-19. We’re still waiting to see the full effects of the pandemic and the government’s responses.

First is Singapore.

The Monetary Authority of Singapore (MAS) is solvent, and over the past few decades proved to be a wise financial regulator.

Unlike insolvent western governments, Singapore’s financial position has been solid.

When accounting for Singapore’s foreign reserves and sovereign wealth fund, the country has net assets well over 100% of GDP.

(Comparatively, let’s review America’s numbers: A 2019 GDP of $21 trillion. But the Social Security shortfall plus the US government’s net worth is NEGATIVE $82.1 trillion.)

And importantly, Singaporean banks are solvent and far more liquid than most western banks. Rather than engaging in risky derivatives trading with customers’ deposits, they keep ample cash on-hand, which minimizes depositors’ risks.

Other countries you could potentially choose for well-capitalized, safe private banks are Liechtenstein and Luxembourg.

Not a single bank in Liechtenstein needed ANY assistance from the state during the 2008 global financial crisis. The country’s banks are conservative and well-run. And the government has zero net debt.

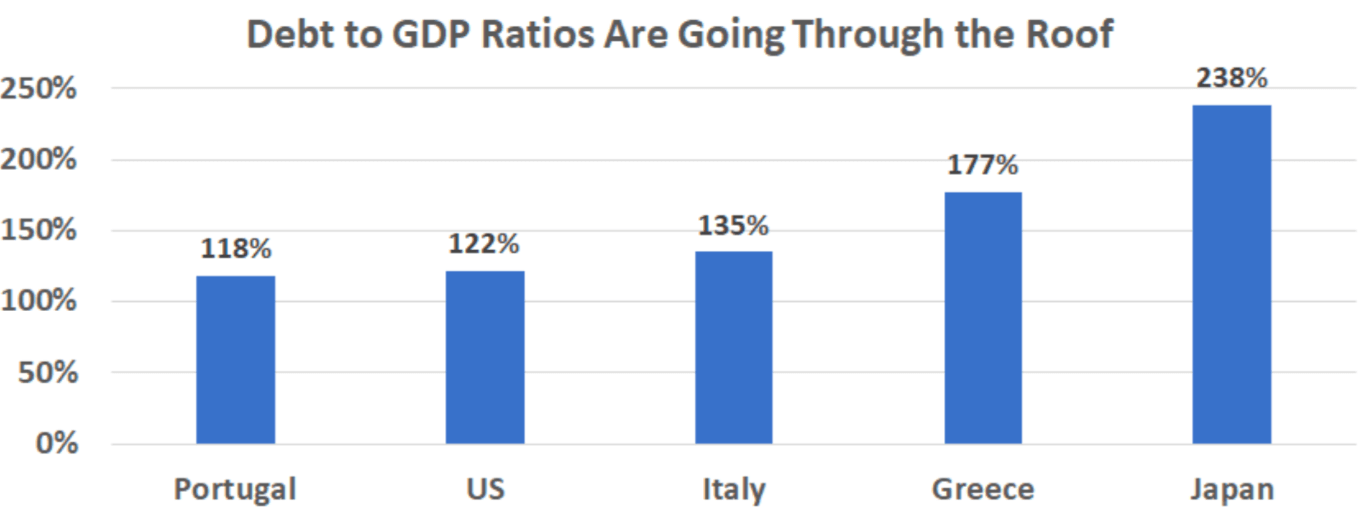

Luxembourg’s banks are backed by a financially healthy government, with a 2019 government debt to GDP ratio of only 22%. (For comparison, the US debt to GDP ratio stands at 122%, and in 2019, Japan’s was 238%.)

(You can read more on these jurisdictions in our “safest bank” section. BUT… keep in mind that as of mid-2020, it’s difficult to understand the exact health of most banking systems around the world.)

Fortunately, if you live in a western country with a subpar banking system, not all of your savings must reside there as well.

It’s the 21st century. You no longer need to choose a bank because there’s a branch near your kid’s karate school. Or because you personally know the bank manager.

Instead, the entire WORLD should be open for your deposits, especially in today’s chaotic economy. We don’t know the full extent of the COVID-19 economic fallout.

We do know, however, that banks will ultimately be on the hook for loan failures. But since banks are opaque, we’ll likely be in the dark… until the bank failures start.

There are still banks around the world that make safety a priority. And if you want to hold some of your savings OUTSIDE the traditional banking system, you have options there, too. (See below for more details on these options.)

Either way, YOU will be in control of your money. You’ll be safe. You’ll be protected.

FREE GUIDE

How To Determine If An Offshore Bank Is Safe

As you’ve learned, not all offshore bank accounts are created equal.

If you are not careful, your new overseas bank account may turn out to be an even worse custodian of your wealth than the risky one across the street.

Learn the exact step-by-step process our team uses to determine if a bank is safe inside this free preview of our in-depth Ultimate Offshore Banking Guide & Comparison.

Inside you’ll learn…

The information in this Offshore Banking Report is from before COVID-19.

We’ll be updating the guide once the new numbers are in.

If you hold 100% of your funds in the same country where you live and work, then you’re taking on some significant legal risk.

Why? You’re holding all of your eggs in one basket.

With an offshore bank account, you’re protected in two ways:

1. Protection from the litigious plaintiffs

Your assets are at even higher risk if you are living in the “Suenited” States – the most litigious country that has ever existed in the history of the world.

In the US, you can be sued over anything and everything. A kid breaks his leg on your front lawn… someone you dated decides to be entitled to your assets… you baked cookies for the school social that had peanut butter and someone decides you owe them hospital money after getting sick.

Suddenly, all of your assets – and all of your life’s savings – are frozen and you’re left without cash to fund your defense… All your assets are up for grabs by frivolous plaintiffs.

Any court or government agency can also freeze you out of your bank account with a single phone call, without any due process and without giving you the chance to make your case.

It’s truly a “guilty until proven innocent” system.

Holding some funds overseas in an international bank account can help provide insurance against this risk. Your home country’s court decisions stop at the border.

2. Protection from government agencies

But court decisions that stop at the border are not your only concern…

Government agencies, too, are a threat. Because governments all over the world are going bankrupt.

Just like individuals, once governments become broke, they become desperate.

Even if you’re completely innocent, you could be ensnared in the government’s dragnet. In many ways, the financial system provides you with no justice. It’s another “guilty until proven innocent” framework.

Whether you’re the target of a government agency or they made a mistake, imagine that you wake up one day to find your entire life savings frozen.

But with some of your savings stashed in a stable, overseas jurisdiction, you’re not completely under the thumb of a desperate government. Your foreign bank account can act as a much needed lifeline.

Over the last few years, interest rates have remained at their lowest levels in the entire 5,000 years of recorded human history.

In the United States, Europe, Japan, etc., safely stashing away savings and maintaining its purchasing power is nearly impossible.

As of this writing, Bank of America (BoA) is paying a whopping 0.06% – just over one twentieth of one percent – annually on deposits.

If your bank pays 0.06%, but the annual inflation rate is 2.3% (as it was in 2019), your savings is losing 2.24% of its purchasing power each year. You need to earn at least 2.3% each year – or even a little more to account for taxes – just to keep up with inflation.

The situation is worse in Europe…

In some parts of Europe, interest rates are negative

Until about a decade ago, negative interest rates were some far-fetched fantasy of central bankers and the banking system.

Since then, negative interest rates have become a reality and are spreading around the world.

Instead of receiving a nominal amount on your deposit, negative interest rates mean that you’re paying the bank for the “privilege” of keeping your money on deposit.

As of April 2020, 80 German banks charge negative interest rates on accounts larger than 100,000 euros. And over a dozen charge negative interest rates to those with less than 100,000 euros on deposit.

But there are jurisdictions around the world where safe, conservative, well-capitalized banks pay MUCH higher interest rates– even on US dollar deposits.

How do you like this article?

Click one of the stars to add your vote...

Other readers gave this article an average rating of 4.8 stars.

Keep some cash and savings at home...

Consider moving at least a portion of your savings into a safe, stable, highly liquid jurisdiction abroad… one that is out of reach of your government and of litigators, and that can weather a financial crisis.

But you don’t have to bank entirely offshore.

In fact, it makes a lot of sense to keep some of your money at home.

You need a transactional bank account to continue paying day-to-day bills. And importantly, in case of a banking crisis where ATM withdrawals are severely limited, several months’ worth of cash in your home safe is a smart strategy.

Do NOT try to use an offshore bank account to evade taxes or hide money… unless you want to spend the next several years turning large rocks into small rocks while wearing a dayglo orange jumpsuit.

Financial privacy is largely dead.

Due to Foreign Account Tax Compliance Act (FATCA) regulations, now literally every financial institution in the world must report their American clients to the IRS.

And while the US did not sign up for the Common Reporting Standard (CRS) – a global tax and information sharing exchange also known as FATCA on steroids – as of June 2020, 108 countries have signed up for this system. All major banking destinations are on the list.

With these reporting mechanisms in place, the risk of getting caught is high… and the punishment can be severe.

But, more importantly…

Illegal tax evasion is not necessary, because there are so many completely legal strategies to slash your taxes

There is a very big difference between illegal tax evasion and completely legal tax reduction and planning.

For starters, US citizens living abroad can claim the Foreign Earned Income Exclusion (FEIE) and earn $107,600 annually, tax-free, in 2020.

And US citizens living abroad also qualify for the Foreign Housing Exclusion. The amount you can save depends on the place you live: The IRS will allow you to deduct more if you’re in Japan, than, say, in Nicaragua. But this amounts to a maximum of another $15,064.

Another option is to take advantage of Puerto Rico’s amazing tax incentives. A few years ago, the government there passed a number of tax incentive laws, the most famous of which are known as “Act 20” and “Act 22”.

(In 2019, Puerto Rico enacted Act 60: the Incentives Code, which consolidated the wide array of incentive programs the territory enacted over the years. Acts 20 & 22 are now part of Act 60, but in this article, we’ll keep calling them by their traditional and more recognizable names.)

Act 20 allows entrepreneurs to start certain types of businesses there and pay just 4% tax.

Act 22 allows individuals to generate unlimited investment income, subject to a few simple rules, and pay zero tax.

So, if you are an investor or business owner, you can use Puerto Rico to slash your taxes to a negligible amount.

If you own a business, consider forming a captive insurance company.

And just about everyone can maximize contributions to an IRA or 401(k).

A conventional IRA, for example, allows you to contribute up to $6,000 if you’re under the age of 50. But if you switch to a 401(k), you can contribute up to $19,500 per year.

If you own a small business, then you’ve got even more options. With a Self-Employed Pension (SEP) IRA, you can potentially contribute up to $57,000 per year for your retirement.

The bottom line is, don’t plan to use your offshore bank account to evade taxes. Use proper, legal tax planning for that.

The absolute “best” offshore bank will be subjective.

Are you looking for a safe banking option?

Or maybe you prefer an offshore account that’s easy to open. This way, there’s very little hassle, and you’ll be sure to move some savings abroad.

With interest rates at historical lows, you could be in search of a competitive interest rate.

Or if you’re a high net worth individual (HNWI), you could be in search of a very secure bank that will protect your sizable deposit.

We’ve unearthed many great banks in multiple jurisdictions that open offshore bank accounts for US citizens and other nationalities.

But here, we’ve winnowed the list down to just five places for you to consider.

In this list, you won’t see classic Caribbean “offshore tax haven” jurisdictions, such as the Cayman Islands or the British Virgin Islands.

Instead, we focus on established, high-quality banks in respectable jurisdictions that are doing business with real people, not just with folks hiding from the tax man.

We’re only naming jurisdictions, not specific banks

There’s a reason we decided to do so…

With so much changing in 2020 (and still changing so rapidly, by the day), we could conduct a thorough analysis of a bank… but then the bank could experience a wave of defaults that impacts its finances.

So, in this article, we decided to only name good banking jurisdictions, not banks in these places.

In early July 2020, I was looking at Bank of America’s financial statements.

Their balance sheet shows $983 billion in loans. And that’s about all the detail you get.

Even doing a deep dive into the footnotes and annual report shows little additional information.

What are the loan terms? What’s the duration risk? How valuable and marketable is the collateral? What legal security was taken over the collateral? Is there even any collateral at all?

We simply don’t know what’s going on behind-the-scenes at banks… especially this year.

And we won’t know the shape of their 2020 balance sheet until annual financial statements are released in early 2021. That means we’ll be in the dark to their financial health for several more quarters.

Meanwhile, just like in 2008, central banks and governments are telling us that everything in the economy is fine, including banks.

Back in 2008, months after officials assured us that the economy would continue to expand, we entered the harshest recession since the Great Depression. The financial system was on the brink of failure.

So, when approaching this subject of “safest” banks, we do so from a position of uncertainty. We simply cannot tell you with 100% confidence that Bank A in Country B will safeguard your deposits.

We can, however, point to jurisdictions that have been safe in the past…

Singapore’s finances have been in order – a balanced budget, often ending up with a surplus, and zero external debt.

Plus, up to this point, the Monetary Authority of Singapore (MAS) has remained solvent.

And generally, Singaporean banks are more consevative than western banks.

In fact, two Singaporean banks we analyzed last year had solvency ratios – the bank’s capital as a percentage of its assets – of 10%. We prefer to see a number of 10% or higher.

But while some US banks might have about the same level of solvency, according to the latest data available, they don’t come close to Singaporean banks’ liquidity.

Both Singaporean banks we analyzed were liquid. In fact, one bank’s liquidity ratio – the bank’s cash and cash equivalents as a percentage of the amount owed to retail depositors – was over 50%. That’s unmatched by most western banks.

As our contacts on the ground affirmed, Singapore was never a coronavirus hot spot. Singapore might withstand the COVID-19 hit.

But in this environment, there’s NEVER a guarantee of safety.

Before opening an offshore account in Singapore, you’ll still need to weigh the risks and conduct your own due diligence.

We can tell you that with most Singaporean banks, premium banking requires a minimum of S$250,000 (~US$180,000) on deposit.

And you’re able to deposit USD, SGD, and several other currencies.

In fact, one Singaporean bank we analyzed allows you to deposit USD, EUR, AUD, CAD, GBP, HKD, NZD, SGD, JPY, THB, NOK, and SEK. This gives you plenty of options and potentially some currency diversification.

But saving in other currencies also exposes you to currency exchange risk. So, you’ll need to weigh the options and decide how much risk you’re comfortable with.

As with most banking jurisdictions, you’ll have to show up in person in Singapore to open the account to comply with Know-Your-Customer (KYC) requirements.

For whatever reason, if Singapore is not a banking jurisdiction that interests you, also consider…

Liechtenstein is a tiny German-speaking principality sandwiched between Austria and Switzerland.

And like its Swiss neighbor, Liechtenstein has long been known as one of the top asset protection and private banking jurisdictions in the world.

The country is rightly seen today as a well-regulated, blue-chip, offshore (technically onshore) destination.

Liechtenstein is in a customs and monetary union with Switzerland, so the country uses the Swiss franc (CHF) as legal tender.

For the past 10 years, the CHF has largely remained stable against the USD. Of course, there’s no guarantee that the franc will retain its value against the dollar. But then again, there’s no guarantee that the dollar will retain its value against the franc, either.

Aside from the currency exchange factor against the USD, the finances of the Swiss government are solid.

And Liechtenstein’s bank’s make their profit by charging fees, not by gambling with their clients’ money. This means that most deposited cash is either conservatively invested or held in their own accounts.

But to open an account there, you’ll need to clear the high account minimum hurdle – $250,000 and up.

In the aftermath of the 2008 Global Financial Crisis, the United Arab Emirates (UAE) 100% guaranteed all deposits – of any amount – for three years.

Covered deposits included those in both local and international banks regulated by the Central Bank of the UAE.

We’re not sure if they’ll do the same thing post-COVID-19.

With oil prices low, most oil-exporting countries dependent on that revenue are hurting. Still, the UAE might have ample savings to sustain their economy. The Central Bank of the UAE (and the entire banking sector there) is backed by the Emirates’ vast oil wealth.

But you also have to consider the instability of the Middle East. The UAE has remained stable, but that could change if a region-wide conflict breaks out.

If you’ve weighed the risks and are interested in the UAE, the minimum deposit for a solvent, liquid bank we analyzed is only 3,000 dirhams (about US$815).

This account is available for non-residents, and to open it, you’ll need to travel to the UAE.

Or, you can look OUTSIDE of the banking system entirely...

Banks don’t have your money segregated and safely stored in the vault.

The second that you deposit your money, it goes out the door to buy bonds and make loans, sometimes to people with less than stellar credit. Your money keeps getting passed around – an IOU of an IOU.

There’s an entire daisy chain, or counterparties, standing between you and your savings.

“Counterparty risk” is the risk that something goes wrong with one of the many, many counterparties in this daisy chain.

One alternative to dodge counterparty risk is to hold 28-day Treasury bills (T-bills), the shortest-dated government debt.

WAIT one second, you might be thinking…

The US government’s debt routinely outpaces its entire economic output (122% debt-to-GDP ratio). That’s a ton of counterparty risk. And it’s true.

Lending money for 30-years – i.e. buying 30-year US Treasury bonds – is absolutely insane.

But we’re reasonably confident that in the next 28 days, the US government won’t default on us. As for the 28 days after that, T-bill holders can reassess the government’s position at that time. At that point, it’s easy to transfer the funds back to a US bank account.

If you’re a US person (a US citizen or resident) and have a US Social Security number, you can buy T-bills through TreasuryDirect.

Another offshore bank account alternative is short-term peer-to-peer (P2P) loans.

For example, you can consider Singapore-based Silver Bullion’s P2P loans.

Silver Bullion customers with gold or silver deposited at the facility can borrow up to 50% of their metals’ value. Their precious metals serve as collateral on the loan.

So if you lend $10,000, the borrower has to provide you with $20,000 worth of collateral in gold or silver.

Using this example, if the value of the gold or silver decreased to $11,000 (110% of the outstanding loan amount at the beginning of the loan), the gold would automatically be liquidated and the lender paid back, with the outstanding balance going back to the borrower.

This is the case throughout the loan – if the value of the gold or silver ever decreases to 110% of the outstanding loan amount, it triggers the same orderly process.

And should a borrower ever default on the loan, the gold is liquidated and you, the lender, are paid back principal and interest in full.

Plus, you can be handsomely rewarded. Silver Bullions’ P2P loans can pay up to 3.5% interest – or 58 times more than the interest on an average savings account.

Bottomline: These P2P loans are an extremely safe way to cut out your exposure to the traditional financial system AND earn interest for doing so.

For more information, you can check out Silver Bullion’s frequently asked questions.

Or read our Ultimate Gold & Silver guide where we discuss this strategy and counterparty risk in more detail…

How you could Double Your Money with an asset

That Has a 5,000 Year History of Prosperity...

Download our FREE precious metals report and learn…

This 50-page report is brand new and absolutely free.

How do you like this article?

Click one of the stars to add your vote...

Other readers gave this article an average rating of 4.8 stars.

If you’re looking for an offshore bank account that’s easy to open, that’s understandable…

Because in some cases, to open a bank account, you’ll have to fill out countless know your customer (KYC) forms and wade through a bureaucratic nightmare.

And you don’t want to make multiple trips abroad or deal with a lot of red tape to secure an offshore bank account.

You’re in luck. You have some options to easily open a bank account, starting with Canada.

Canada is NOT the place to park large sums of cash.

For the most part, like many US banks, Canadian banks are not well capitalized or very liquid. The Canadian Deposit Insurance Corporation only has a reserve of C$5.0 billion to insure C$807 billion in deposits.

All that said, if you’re just dipping your toes into offshore banking, Canada might be a convenient place to consider.

To open an account, you’ll need to show up at a bank branch. Gone are the days when you could open bank accounts from your living room.

But if you’re an American, traveling to Canada likely is not a problem. You have just a short plane ride to Toronto for those on the east coast or to Vancouver for those in the west. Some Americans can even take a short drive over the border.

And once you arrive, you’ll find the account opening process simple and straightforward.

The bank we analyzed in eastern Canada only requires two pieces of identification for any nationality. So, your passport and driving license should be enough. But don’t forget to double-check these requirements before heading to Canada.

Another plus: Some Canadian banks will allow US dollar-denominated accounts.

But keep in mind that while the Canada Deposit Insurance Corp (CDIC) insures up to C$100,000 per eligible account, they will not compensate an account in a foreign currency (including in USD).

Depositing relatively little money in a Canadian account will also relieve Americans from FBAR reporting (assuming you have less than $10,000 in aggregate value across various financial accounts outside of the US).

So, consider Canada as an easy place to open an offshore account. It’s NOT a country for large deposits. But if you’re just looking to diversify your savings and open your first offshore bank account, Canada could be a good place to start.

Or, if you’re willing to travel to a less-known destination, they, too, have an incredibly easy account opening process…

In many cases, when you open a bank account somewhere in the world, you’ll fill out countless documents. You’ll present your other existing bank account information.

The bank will have strict requirements for proof of address. You might wait for a couple of hours to open an account.

But in the Republic of Georgia, all this goes out the window…

In fact, one of the easiest offshore bank account experiences of my life happened in Georgia.

(This is telling. I’ve traveled to over 130 countries. I have multiple bank accounts worldwide. I even own my own bank.)

You can stroll into a Georgian bank with your passport and very little money. (Currently, the minimum deposit at one bank is only 10 Georgian lari – about US$3.25.)

And that’s it. You’re on your way to an offshore bank account… likely in less than half an hour.

Bank officials will ask you for an address. But they won’t ask for proof. You might find that the bank’s system can’t handle an address that’s different from your passport.

So, if you’re an American living in Thailand, the bank employee will ask you for a US address. In this case, an address of your relatives living in the US will work – again, there’s no check.

(Americans – you’re still on the hook for US government reporting, no matter where you live. If the total value of your foreign financial accounts exceeds $10,000 at any time during the calendar year, you must fill out FinCEN 114 – the Report of Foreign Bank and Financial Accounts (FBAR).

Also, depending on your marital and residency status, you may have to also file an IRS Form 8938, which is the Foreign Account Tax Compliance Act (FATCA) reporting form.)

But while the opening procedure is simple, traveling to Georgia – one of the safest and least corrupt countries in the world – is more involved.

Georgia is a small country, and you’ll have a couple of layovers before landing there. And when you finally land, it could be at 3:00AM – a common arrival time for international flights.

But you may find that the trip is well worth it.

On top of an easy account opening experience, Georgia’s banking sector has been safe.

Total deposits across the banking sector – when compared to the country’s GDP – are low, making it possible to bail out Georgia’s banks, if needed.

Both Georgia’s government and its central bank are solvent. A debt-to-Gross Domestic Product (GDP) ratio of 41.3% for the latest fiscal year indicates that the country’s debt level is manageable.

Georgia’s central bank solvency is 19.6%, which is a good margin of safety.

Note that Georgia only has a small amount of deposit insurance protection – 15,000 Georgian lari, or about US$5,000. So if your Georgian bank fails, you can indeed lose your deposit over this amount…. unless the government bails out the bank.

In the past several years, Georgia has been a stable banking jurisdiction. And we’ve been confident in the Georgian banking system.

But COVID-19 changed everything… and we won’t know any more information about Georgia’s banks until their comprehensive annual reports are released in early 2021.

How To Open A Safe Offshore Bank Account

the EASY Way...

We’ve done all the hard work and analyzed 32 banks in 22 different jurisdictions. Whether you are looking for the safest account, want to open an account without leaving home or want to earn higher interest– we’ve got you covered.

Members of our flagship intelligence service, Sovereign Confidential, have access to all of that (and much more) inside our Ultimate Offshore Banking Guide & Comparison.

You can download a free preview of this in-depth report here..

Inside the preview you’ll find…

The information in this Offshore Banking Report is from before COVID-19.

We’ll be updating the guide once the new numbers are in.

Wells Fargo offers a “Way2Save” savings account that pays a big fat 0.1% interest rate.

But in the Land of the Free, interest from your bank account is TAXABLE. So after accounting for taxes, you’re looking at around 0.08% interest.

Meanwhile, the annual rate of inflation for 2019 was 2.3%.

So, to figure out your “real rate” of interest, take your “nominal rate” of 0.08% minus the rate of inflation of 2.3%, for a grand total of… NEGATIVE 1.5%.

When you’re guaranteed to lose money, you don’t have a savings account. You have a dwindling account.

Even supposedly “high-yield” accounts at Marcus by Goldman Sachs offer only 1.05%. But at that rate, you’re still guaranteed to lose money.

However, interest rates are not near zero in all jurisdictions.

Historically, certain countries like Georgia and Mongolia – which is not our favorite banking jurisdiction – have featured higher interest rates.

In Georgia you can earn 10.3% interest on a 24-month certificate of deposit (CD).

But don’t let the high interest rate alone prompt you to open a CD in Georgia. Because to earn that 10% rate, you must hold your deposit in Georgian lari, not US dollars.

But by holding Georgian lari in a bank account, you’re taking on currency exchange risk. Post-COVID, the lari has fallen 9.7% against the USD. There’s a chance that the lari could appreciate from here. Or it could lose further value against the USD.

Alternatively, you could choose to denominate your savings in USD. A 12-month CD in Georgia was recently paying out as much as 3% a year to non-residents.

All that said, if you want a high interest-yielding Georgian CD – whether denominated in lari or USD – you must be comfortable with the risks.

And with interest rates around the world slammed to the floor, at the moment, we cannot point to a bank that’s both ultra safe and offers a competitive interest rate.

But there is still a great non-financial system solution: Peer-to-peer (P2P) loans at Singapore-based Silver Bullion.

When you loan money to someone who has gold or silver deposited at Silver Bullion’s facility, their precious metals serve as collateral on the loan. The interest rate varies, based on the supply of loans and demand for loans. (Check out Silver Bullion’s website for the latest rates.)

So, P2P loans are an extremely safe way to both cut your exposure to the traditional financial system AND earn interest.

We briefly wrote about P2P loans in the safety section. This link will take you back up to that section, where you can read more.

If you are looking for yield and safety, we think this option makes a lot of sense right now.

You can learn more about this option inside our Ultimate Gold & Silver Guide that you can download here.

With salaries almost double that of its neighbors, Liechtenstein handpicks the best people from Swiss banks to work for them.

Liechtenstein is also exclusive with its banking customers.

The country does not bother providing transactional banking to non-residents and focuses instead on high-end services (but does that extremely well).

Translation: You need to be a High Net Worth Individual (HNWI) to consider Liechtenstein, as they only deal with big money.

The minimum deposit requirements we have seen in the country start at $250,000.

That said, if you are looking for a private bank, Liechtenstein might be a frontrunner.

Historically, Singapore has not only been a safe banking destination.

It’s also a jurisdiction for high net worth individuals.

As we highlighted before, for most Singaporean banks, you’ll need S$250,000 (~US$180,000) on deposit.

You might be able to initially deposit less money. But note that some Singaporean banks will charge a monthly fee – about US$50 – if your account balance is lower than S$250,000 or the bank’s specific, stated minimum.

You’ll find that in return for clearing this hurdle, some banks will extend you a highly personalized banking experience. So, you’ll be much more than an account number.

We’ve analyzed dozens of offshore banks in over 20 banking jurisdictions...

If you are already a member of our flagship international diversification service, Sovereign Confidential, you can find our latest Worldwide Offshore Banking Review in your member area.

Inside you will find a much more in-depth analysis of dozens of banks in over 20 banking jurisdictions.

By reading this report, you will learn which banks are the world’s safest, which banks pay higher than average interest rates on CDs (3% in USD and even more in local currencies).

Yes, even Americans can open offshore bank accounts. It’s sometimes even possible to do it remotely, without leaving the comfort of your living room.

To set up an account, most banks around the world require you to visit their branch in person. This is called personal presence.

Sometimes the process can be quite simple, requiring just a passport and 30 minutes of your time, and sometimes you must jump through many hoops.

The requirements vary from country to country and from bank to bank. Always inquire with the bank itself before making a trip to make sure you bring the correct documents.

Here’s the list of the most common documents:

Important Tip:

When opening an offshore bank account, it’s important not to give up if you get denied. Go to another branch of the same bank – they may have more experience working with foreigners and will happily take you onboard.

We have seen that happen to us a few times in various countries.

Always try two or more branches of the same bank.

How To Open A Safe Offshore Bank Account

the EASY Way...

We’ve done all the hard work and analyzed 32 banks in 22 different jurisdictions. Whether you are looking for the safest account, want to open an account without leaving home or want to earn higher interest– we’ve got you covered.

Members of our flagship intelligence service, Sovereign Confidential, have access to all of that (and much more) inside our Ultimate Offshore Banking Guide & Comparison.

You can download a free preview of this in-depth report here..

Inside the preview you’ll find…

The information in this Offshore Banking Report is from before COVID-19.

We’ll be updating the guide once the new numbers are in.

Once again, banking offshore is 100% legal.

Not only is it legal, it’s a smart thing to do. BUT, depending on your home country, there may be disclosure forms to file with your tax authorities.

This is where people run into trouble with foreign bank accounts: Whether intentionally or not, they fail to disclose the account. And some countries take those violations seriously.

The United States is one of them.

If you are a US citizen, US green card holder, or a legal alien (foreigner living in the US), and have a foreign bank account, you may need to file the following forms:

1. FinCEN Form 114 (also known as the FBAR)

US taxpayers who have a financial interest or signature authority over foreign bank or financial accounts must file this form if the aggregate value of those accounts exceeded $10,000 at any time during the calendar year.

This form includes bank accounts, but also other foreign financial accounts such as a foreign brokerage, or even an offshore precious metals account.

The FBAR must be filed electronically each year by April 15th at this website.

2. IRS Form 8938 (FATCA-related reporting)

This form is required for US taxpayers who hold certain foreign financial assets, including bank accounts, brokerage accounts, and shares of private companies.

The reporting threshold is MUCH higher than the FBAR, and depends on two factors—whether or not you’re married, and whether or not you live in the United States.

For example, a single person living in the United States must file the form if his/her foreign financial assets exceeded $50,000 on the last day of the tax year, or $75,000 at any point during the year.

But a married couple living overseas doesn’t need to file the form unless their foreign financial assets exceeded $400,000 on the last day of the tax year, or $600,000 at any point during the year.

Form 8938 should be filed along with your usual IRS form 1040 tax return.

3. IRS Form 1040 Schedule B

US taxpayers with a foreign bank account should also file a 1040 Schedule B, and check the box in Part III where it asks about foreign financial accounts.

4. Canadian Offshore Banking Disclosure forms

Canadian citizens, if you have “specified foreign property”, which includes foreign bank accounts, and total value exceeding CAD $100,000, you’re obliged to disclose those assets to CRA on form T1135.

Videos & Step-By-Step filing instructions.

If you are already a member of our flagship international diversification service, Sovereign Confidential, you can find step-by-step instructions on how to file all of these forms in your member area. We will also notify you of all the deadlines in advance.

You can keep 100% of your savings at banks in your home country – institutions that never miss an opportunity to treat you like a criminal, gamble with your money, and reward you with, in 2020, at best a “high yield” interest rate of maybe 1% on your savings.

If this bank goes under, you will have to foot the bill – through taxes in case of a bail out, or by saying goodbye to your deposit in case of a bail in.

If you find yourself on the wrong side of some government agency’s list – even if by mistake – you can be frozen out of your account in an instant, depriving you of the funds you need to put food on the table for your family.

And if you live in the US or one of many other western countries, chances are this bank will be illiquid, insolvent, and headed by a team of executives with insane compensations and very low moral standards.

OR…

You can look for other banking options abroad.

Safer options. Banks that will actually welcome you as a customer. A bank that will pay you more than a miserly rate of interest, located in a jurisdiction with zero-to-low debt and a strong, well-capitalized deposit insurance fund.

And this account might even pay you a solid interest rate – one that’s well above the rate of inflation, and that actually puts money in your pocket year after year.

The choice between the two is a no-brainer.

And if you’re concerned about the banking system, there are still solutions to safeguard your savings completely outside of banks. The shortest-dated T-bills and P2P loans backed by collateral are two solutions we presented here that make a lot of sense.

In our world full of risks, you can take back control of your savings with an offshore bank account.

How you could Double Your Money with an asset

That Has a 5,000 Year History of Prosperity...

Download our FREE precious metals report and learn…

This 50-page report is brand new and absolutely free.

Sovereign Confidential is our flagship intelligence report service informing you about the best places on Earth to safely protect your life, your liberty and your assets.

Our intelligence reports cover everything from new residency or foreign banking options to how to reduce, defer, or even eliminate your taxes, to incredible investment picks.

Members have recently received our latest Ultimate Offshore Banking Guide & Comparison, where we did an in-depth analysis on over 20 offshore banks and banking jurisdictions.

Inside you will learn which banks are the safest in the world, which pay the highest interest (over 3% in USD and even more in local currencies) and how exactly you can open an offshore bank account without leaving home.

Sovereign Blueprint is your essential introduction to international diversification, a guide to ensure you have access to the most important tools to build your own Plan B.

With Sovereign Blueprint, you’ll learn…

Join over 100,000 subscribers who receive our free Notes From the Field newsletter, where you’ll get real boots-on-the-ground intelligence as we travel the world and seek out the best opportunities for our readers.

It’s free, it’s packed with information, and best of all, it’s short… there’s no verbose pontification here – we both have better things to do with our time.

And while I appreciate all the visitors who stop by our website, I provide special bonuses to our email subscribers… including free premium intelligence reports and other valuable content that I only share with them.

It’s definitely worth your while to sign-up, and if you don’t like it, you can unsubscribe at any time with just one click.

How did you like this article?

Click one of the stars to add your vote...

Other readers gave this article an average rating of 4.8 stars.