April 11, 2013

London, England

[Editor’s note: Tim Price, Director of Investment at PFP Wealth Management and frequent Sovereign Man contributor is filling in while Simon is viewing agricultural property today.]

These are certainly days of miracle and wonder. Well, of absurd and extraordinary financial experimentation, at any rate.

Last week, for example, saw the Bank of Japan abandon any last pretense of restraint and topple headfirst into a gigantic pile of monetary cocaine.

The scale of the policy is daunting: the Bank of Japan intends to double the country’s monetary base over two years via the aggressive purchase of long term bonds.

It would be difficult to overstate the drama of this monetary stimulus(although we favour the word debauchery).

Yet as the Japanese monetary authorities declare a holy war against deflation, it would only be fair to draw attention to the colossal opportunity being presented as the antidote to monetary intemperance, namely gold and gold miners.

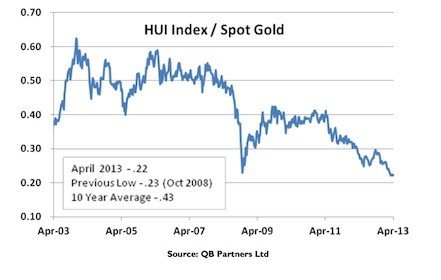

There is a clear mismatch between the prices of gold and silver mining shares and spot prices of gold and silver. But as to why the miners are trading so poorly relative to the physical is unclear to us.

It may be because the market expects the price of gold and silver to fall (not a belief to which we subscribe, given current monetary events for example in Japan).

It may be because the rise of gold exchange-traded funds has removed a natural bid for shares of the miners.

And it may be because the market is waiting for goldbug hedge fund manager John Paulson to capitulate on his own holdings of precious metal mining stocks.

Nobody knows. We are merely content to play the long– and rational– game.

As Lee Quaintance and Paul Brodsky of QB Partners point out, “the ratio [Mining share prices to spot gold] is again at its ten year weekly low. If there is any remaining validity to the merits of investing in financial assets based on historical value, this would be the time to buy miners.”

They go on to add (and we concur),

“Our strong bias is that prices of bullion will rise significantly. Selling the miners at current absolute and relative valuations would be tantamount to throwing in the towel on the entire concept of value investing, now and in the future.”

“The reality is that we cannot be 100% sure of the outcome from all the monetary mayhem in Europe, Japan and the US, and we do not have a good sense of timing if and when our outcome proves correct. . . All we can do is try to recognize value within the context of current and extrapolate-able events.”

We agree that the temporary weakness of the price of bullion is a buying opportunity in light of Japan’s vast money-printing experiment. And the same likely holds for the price of gold mining companies.

Bear in mind, though, that as the money printing ritual goes on, the prices of everything are being so grievously distorted. Doubt is uncomfortable in this environment. But certainty is absurd.