It was just weeks ago that the US government barely averted a debt ceiling shutdown with a last-minute bill to kick the can down the road until December.

This gave them 2 months to tackle a problem that’s been decades in the making, with a debt that now totals nearly $19 trillion.

So far the solutions they’ve come up with have been nothing short of comical.

In fact the very first ‘solution’ introduced in a bill earlier this month was designed to give Congress special powers to kick the can even further down the road. Genius.

Then there was a bill proclaiming to “take the possibility of default off the table” by promising that the government’s mandatory obligations would be paid first.

Wow. It’s so pathetic that the government needs to actually pass a law just to reassure the rest of the world that they’ll pay their debts.

It’s like being flat broke and telling your landlord, “Don’t worry, I know I don’t even have enough income to feed myself, but as soon as I get some money, I’ll pay you first.”

Hardly reassuring.

But the grandest ‘solution’ of all thus far has been the Debt Ceiling Alternative Act, introduced on October 9th.

This bill would authorize the President of the United States to liquidate government assets in order to raise cash the next time they breached the debt ceiling.

Candidly, this is what everyday people have to do when there’s too much month at the end of the money. They liquidate. They have garage sales. They pawn their car title.

There’s just one problem: it turns out the government really doesn’t have too many high quality assets to offer.

The text of the Debt Ceiling Alternative Act actually lists WHICH government assets should be sold off. And it ain’t pretty.

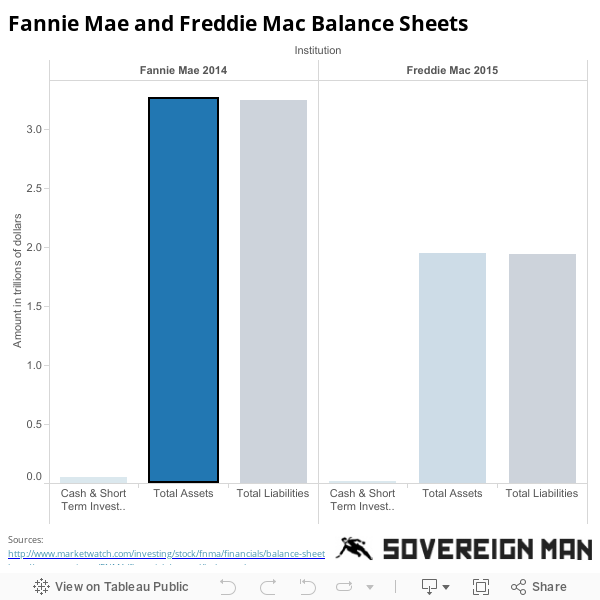

Topping the list, in fact, are the non-performing mortgages of Fannie Mae and Freddie Mac.

If you’re not familiar, these are home loans owned by quasi-government agencies that are currently in default!

That’s pretty pathetic– the best thing the government can offer up to pay its debts is a pool of deadbeat mortgages. These aren’t exactly assets that investors would pay top dollar for.

The list goes on to include other mortgages and properties owned by these same federal housing agencies.

Problem is, Fannie Mae and Freddie Mac are already just a hair away from insolvency.

And given that the federal government is on the hook to guarantee Fannie Mae and Freddie Mac, picking through their balance sheets like hungry vultures would essentially trigger a government bailout.

So whatever money the government would raise by selling off Fannie Mae and Freddie Mac assets would have to be injected right back into the companies to bail them out of insolvency.

It’s genius!

In the final analysis, it’s clear the government simply doesn’t have the assets to finance itself.

Sure, they’ve been successful at kicking the can down the road for now. But some day they are going to need serious help.

And who’s going to be there to bail them out?

You. Whether you like it or not, whether you agree or not.

That is, if your assets and savings are within their reach.

They will take everything they can get their hands on to help keep themselves afloat, resorting to time-eternal government practices of capital controls and confiscation to do so.

Thus, it’s up to you whether you want to foot the bill for decades worth of their bad decisions.

If you do, feel free to leave everything you have in the country for them to take.

If you believe that nearly $19 trillion in debt makes for a consequence-free environment, there’s nothing you need to do.

If not, consider moving at least a portion of your assets and savings outside of the country and to put them into stable, secure jurisdictions abroad.