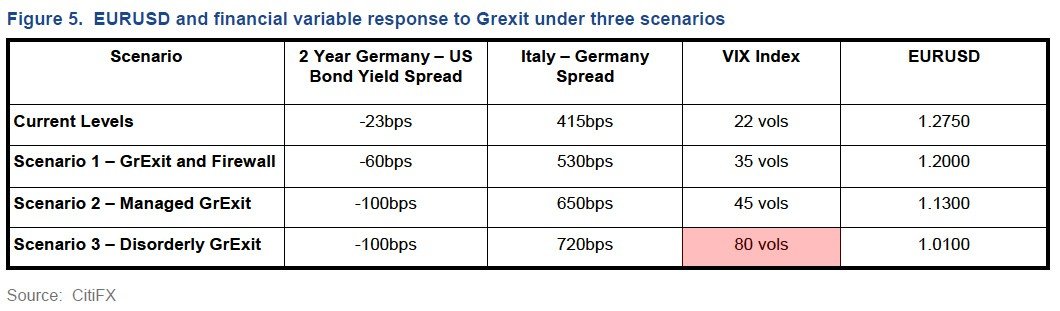

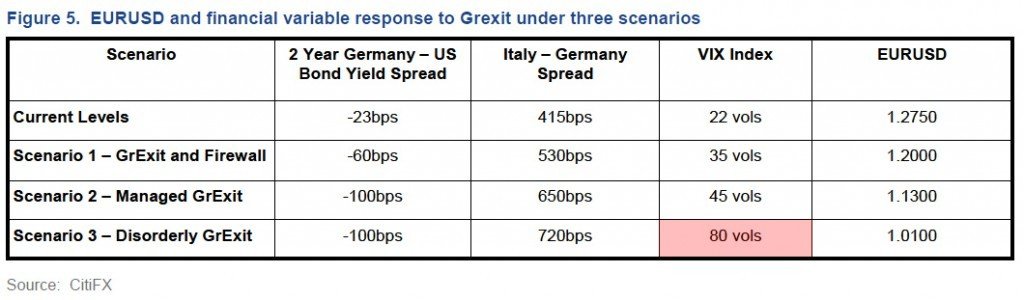

Everyone is pretty aware of the terrible situation Greece is in and with their newly elected anti-bailout leadership, it’s highly likely that they will leave the EU. In a recent analysis of the situation, Citi has released a mock up of three scenarios with the most disastrous being a “Disorderly GrExit”. In that scenario the VIX index, which indicates volatility, would reach 80 vols, a number not seen since the 2007 crash. CitiFX reports:

“1/ Managed Grexit with firewall in place but insufficient to remove EMU break up risk or risk aversion: Our analysis suggests that EURUSD can drop to 1.2000 under this scenario (Figure 5). We expect both VIX to move higher to 35vols and BTP yields to temporarily break above 600bp (Figure 5). In ‘International Interest Rate Strategist from 17 May 2011 Citi’s rate strategists published estimates of German bond yields that are theoretically with unchanged probability of EMU break-up as well as a spike in global risk aversion. In particular, German 2y yields which currently stand 6bp could trade as low as -35bp. In the case of the Bund yields, our rate strategists estimate a drop to 85bp from current 143bp. The BTP-Bund yields spread and Germany-US 2y bond yield spread are expected to widen/ tighten from current levels (Figure 5). Importantly, both Italy-Germany bond yield spread and VIX are expected to remain below their 2011 highs.

“1/ Managed Grexit with firewall in place but insufficient to remove EMU break up risk or risk aversion: Our analysis suggests that EURUSD can drop to 1.2000 under this scenario (Figure 5). We expect both VIX to move higher to 35vols and BTP yields to temporarily break above 600bp (Figure 5). In ‘International Interest Rate Strategist from 17 May 2011 Citi’s rate strategists published estimates of German bond yields that are theoretically with unchanged probability of EMU break-up as well as a spike in global risk aversion. In particular, German 2y yields which currently stand 6bp could trade as low as -35bp. In the case of the Bund yields, our rate strategists estimate a drop to 85bp from current 143bp. The BTP-Bund yields spread and Germany-US 2y bond yield spread are expected to widen/ tighten from current levels (Figure 5). Importantly, both Italy-Germany bond yield spread and VIX are expected to remain below their 2011 highs.

2/ Managed Grexit with firewall implemented in response to Grexit: Our analysis suggests that EURUSD can drop to 1.1300 under this scenario (Figure 5). We expect both VIX and BTP yields revisit their 2011 highs. In ‘International Interest Rate Strategist from 17 May 2011 Citi’s rate strategists also published estimates of German bond yields that are theoretically consistent with a 5-10% increase in the probability of EMU break-up (estimated to be 19% at present) as well as a spike in global risk aversion. Under this scenario, the German 2y yields could trade as low as -75bp while the Bund yields could drop to 70bp. The BTP-Bund yields spread and Germany-US 2y bond yield spread are expected to widen/ tighten considerably as a result (Figure 5).

We suspect that any further significant escalation in the euro zone debt crisis could be met with a concerted policy action by all major central banks. In turn this is likely to add to the downside pressure on the short-term government bond yields across the board. In addition, one could argue that escalating demand for safe haven could push US treasury yields temporarily below zero and thus result is somewhat less negative Germany-US 2y bond yield spread. The impact on our projection need not be that great given the relatively small size of the beta coefficient. For example, a drop in the 2y rate spread to only -50bp will mean that EURUSD would fall by 0.4bf instead of our original projection of 1.2bf.

3/ Disorderly Grexit with excessive volatility in other markets: Our analysis suggests that EURUSD can drop to 1.0100 under this scenario (Figure 5). We deem this scenario much less likely than the previous two given that the policy response by global central banks and policy makers is likely to be swift. We nevertheless decided to include the scenario to provide a worst case estimates. In particular, we keep our assumption for German rates but expect that the BTP yields surge to 800bp leading to further widening in the spreads to Germany to 730 bp. We also assume that VIX moves closer to its Lehman highs (Figure 5). We have to admit that the assumption regarding the BTP yields is somewhat arbitrary. BTP yields surged well above 800bp in the years before the introduction of EUR.”