Alternative Investments

Ultimate Guide 2022

-

AUTHOR

Harrison Burge -

PUBLISHED

March 2, 2021

Are you concerned with how overvalued the stock market has become? Do you see investors and speculators taking outsized risks to achieve modest returns? Is there a better path — a way to take much less risk but still achieve satisfactory returns?

In this guide, we’ll explain how you can take advantage of alternative investments to achieve market-beating returns in 2022 and beyond…

Donec id elit non mi porta gravida at eget metus. Nulla vitae elit libero, a pharetra augue. Etiam porta sem malesuada magna mollis euismod. Praesent commodo cursus magna, vel scelerisque nisl consectetur et. Curabitur blandit tempus porttitor. Nulla vitae elit libero, a pharetra augue.

Donec id elit non mi porta gravida at eget metus. Nulla vitae elit libero, a pharetra augue. Etiam porta sem malesuada magna mollis euismod. Praesent commodo cursus magna, vel scelerisque nisl consectetur et. Curabitur blandit tempus porttitor. Nulla vitae elit libero, a pharetra augue.

Donec id elit non mi porta gravida at eget metus. Nulla vitae elit libero, a pharetra augue. Etiam porta sem malesuada magna mollis euismod. Praesent commodo cursus magna, vel scelerisque nisl consectetur et. Curabitur blandit tempus porttitor. Nulla vitae elit libero, a pharetra augue.

If you don’t feel comfortable with overvalued stocks and the insanity of financial markets in 2022, you don’t have to stay 100% invested in the stock market. You have other options.

In this article, we’ll discuss some other investment options (click to go to the respective section and read more):

Please note that the below content is intended for informational purposes only.

We are not financial advisors, and this article should not be construed as investment advice. Always consult with a financial advisor who’s familiar with your goals, appetite for risk, investment timelines, etc. before making any investment decisions.

Learn EVERYTHING you need to know about

buying, owning, storing and investing in gold & silver…

Download our FREE precious metals report and learn…

This 50-page report is brand new and absolutely free.

In this section we'll cover:

“Here [at Sovereign Man], we continue to think of stocks as small parts of businesses, not wiggly lines that move up and down your smartphone or computer screen when you log into your trading App or brokerage account, depending on the day-to-day liquidity and supply and demand for the stock.”

— Tim Staermose, Sovereign Man Chief Investment Strategist

There’s a specific purpose for selling a company’s equity (i.e. company shares)…

Or issuing a corporate bond…

It’s to raise capital for productive businesses.

Unless an entrepreneur has his or her own capital, they need early-stage investors. And in exchange for supplying capital and taking a calculated risk, these early-stage investors will receive company shares, bonds or convertible notes (bonds that convert to company shares at a predetermined time).

Before seeing a return on their investment, early-stage investors will often have their capital tied up for a year or longer. So, by committing to this new business venture, early investors are missing out on other opportunities. (This is referred to as the investor’s “opportunity cost.”)

Therefore, a long-term reward needs to be in place for early-stage investors…

Sometimes, this reward is an initial public offering (IPO).

An IPO will ideally give early-stage investors a much higher share price than their original entry price. But a successful IPO also gives these individuals access to liquidity. Those who need or want to sell their shares can do so, quickly and easily, with the click of a mouse on an exchange like Charles Schwab, E*Trade, etc.

(This is not Sovereign Man’s endorsement of certain stock exchanges. Before you open an account, complete your own thorough due diligence about the exchange.)

And the publicly-traded stock market provides another useful function…

New investors who did not originally buy pre-IPO shares can own a portion of the business. They will likely not pay the pre-IPO price for their shares.

Still, if the business is profitable and its future looks promising, an investor on a publicly-traded exchange can take a calculated risk. (Just like the early investor did previously.) As Tim emphasizes above, the investor can own a small part of the business.

In fact, disciplined investors who identify companies in a steady or growing industry, with low or no debt, improving margins and solid management who are incentivized not as managers, but as owners… can achieve long-term success in the stock market.

But over the past few years, the stock market has become untethered from reality…

The stock market is no longer about picking well-managed companies with high quality assets.

Nearly ALL stocks have been rising; even companies like Coca-Cola, while their businesses are shrinking and revenues are declining. And a large percentage of investors are blindly piling in to buy those stocks.

Clearly, many investors — both individuals and financial institutions (hedge funds, asset managers etc.) — are not taking a “bottom-up”, value-driven approach. These so-called “investors” are not rolling up their sleeves and putting in the work and hours. They’re not scouring disclosures like annual 10-K filings. They’re not running financial models to consider future cash flow.

Instead, the stock market and many investors are completely beholden to central bankers.

It seems all that matters is whether central bankers will conjure more money out of thin air, and if a portion of that money will wind up in financial markets.

This easy money from the Federal Reserve has turned the stock market into a casino.

And investors — high on that monetary dopamine — are doubling-down on the hope that central bankers will continue to succeed in pushing asset prices higher.

In a way, they’re handing out free money by engineering gains for everyone holding stocks. And it’s possible that this insanity continues for a few more years.

But if you examine the relevant metrics, valuations are already severely stretched…

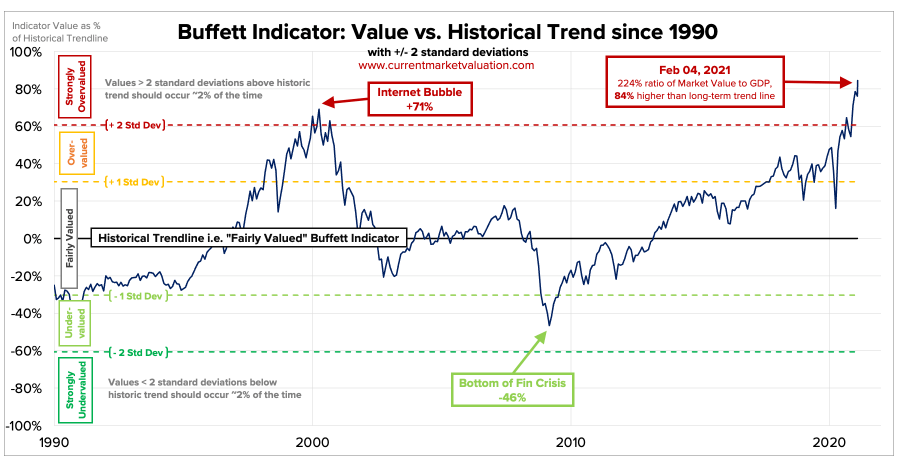

For example, there’s the total market capitalization of US stocks divided by the US Gross Domestic Product (GDP), to name but one such indicator.

(Market capitalization — or market cap, for short — is a company’s net worth. So, total US market capitalization is the combined value of American publicly traded companies. And GDP is an aggregate measure of consumer, investment and government spending, plus net exports (exports less imports) — or the country’s total economic output.)

Total Market Capitalization to GDP is known as the “Buffett Indicator” — because of billionaire investor Warren Buffett’s affinity for this ratio. When the ratio is lower (like in the early 1990s and after the sharp decrease during the 2008 Global Financial Crisis), it indicates that stocks are in value territory. And when the ratio is high, like today, it reveals that stocks are overvalued.

The Buffet Indicator’s “Fairly Valued” range is between -20% and 20%. That is, when the aggregate value of stocks is one standard deviation above or below America’s GDP.

But we’re nowhere near the Fairly Valued range today.

As the chart below indicates, the Total Market Cap to GDP is over 220%. That’s over 80% higher than the long-term trend line — and even higher than the Dotcom bubble’s ratio in the early 2000s.

And it’s not just the Total Market Capitalization to GDP that reveals an overvalued stock market.

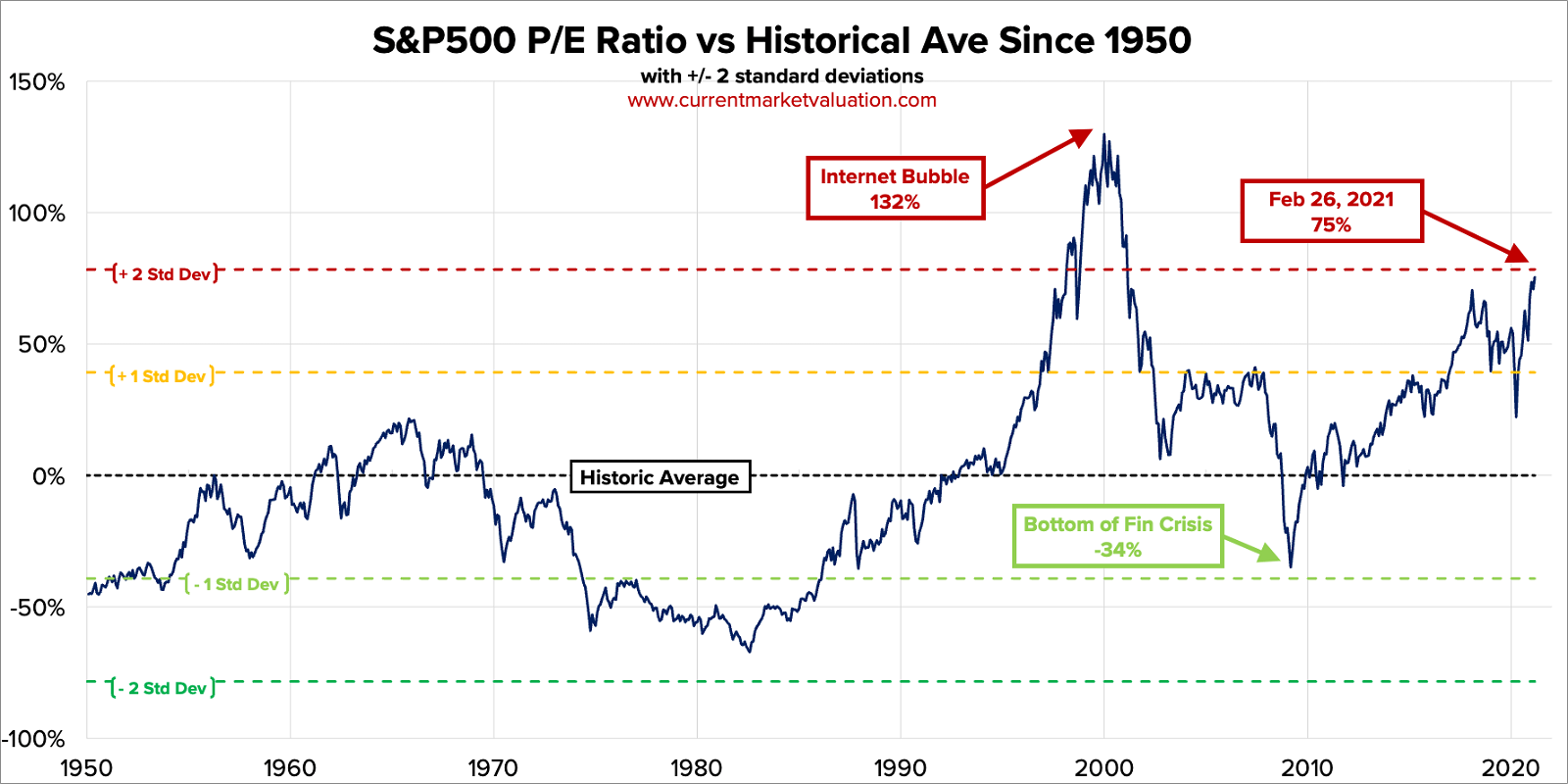

Let’s review the price to earnings ratio (P/E) of the S&P 500 — the 500 largest US stocks by market capitalization. (The price to earnings ratio reveals how much investors are willing to pay (i.e. the “multiple”) for every dollar of company earnings.)

By this metric, over the past 70 years, the stock market has only been more overvalued once: during the Dotcom bubble.

Such high valuations — both for the Total Market Capitalization to GDP Ratio and the S&P 500 P/E Ratio — reveal the abandonment of sound, traditional investing principles.

Again, we don’t know or pretend to know how much longer this can go on. Months? Maybe. Years? Possible.

What we do know is this: Bubbles end… and they end especially badly for investors who entered markets near the top. And when they do, it can potentially take decades to recover losses.

Japan’s stock market is a prime example…

In December 1989, Japanese investors were in a frenzy. The country’s Nikkei Index — comprising the top 225 Japanese companies by market cap — soared to an all-time high of 38,957.

But then, fearing rising debt levels and coming inflation, Japan’s central bank hiked interest rates. Less than one year after the blow-off top, the market’s value was cut in half.

Over the past few decades, Japanese policymakers attempted to reinflate stock prices. But it wasn’t until mid-February 2021 that the Nikkei Index finally hit a milestone: back above 30,000.

This is still 30% below the all-time high.

The lesson: If you had invested in the Nikkei Index in 1989 at the market top, over 30 years later you would still hold a losing trade.

The US stock market is not immune to this same pattern.

We’re not investment professionals, so we’re not here to offer advice. And we’re also not market prognosticators.

But we can point to the facts and urge you to think about the risks in this market.

When sound investment practices have been thrown out the window, it’s the time to pause, reflect and potentially consider investing in other assets. (Your investment advisor can speak with you about your specific needs, diversification strategy, risk appetite and timelines.)

We’ve already cited some metrics that show that US stocks are in overvalued territory.

But anecdotes are helpful, too.

And for a recent example of stock market absurdity, let’s review what happened with GameStop in early 2021…

The GameStop short squeeze of 2021

If you followed the financial news in early 2021, you will likely have caught the story of the GameStop short squeeze.

But let’s start with the basics; with a little bit of a background on the companies, individuals and institutions that collided to create some proverbial market fireworks.

GameStop Corporation (GME on the New York Stock Exchange) sells video games in DVD format.

The business has over 5,500 stores around the world. And it generates almost all its sales from these locations. That business model worked really well… in 2005.

But today, most users download video games online directly from the publishers, or they stream games from Google, Amazon, Apple, or Steam. Going into a store and buying a DVD is a thing of the past, and GameStop’s sales have suffered as a result of this trend.

A handful of hedge funds noted what seemed obvious: GameStop would continue bleeding cash. And eventually, the company would go out of business. So, these hedge funds “shorted” GameStop, or in other words, bet that GameStop’s share price would decline. (Again, we’ll detail more specifically how these funds “shorted” GameStop’s stock below.)

But little did the hedge funds know that lurking on Reddit, an Internet message board, was a discussion heating up in the “Wall Street Bets” channel.

These individual investors — also called retail investors — went on Reddit and basically said, “Enough is enough. We’re tired of hedge funds exploiting the market.”

So, the little guys — the Davids of the story — banded together, spread the word online, and used their collective power against the Goliath hedge funds. These retail investors — many of whom use the popular Robinhood trading app — successfully bid up the price of GameStop’s stock to absolutely epic levels.

In fact, GME’s stock price skyrocketed from $17 per share in early January to an intraday high of $450 in late January — all due to these small investors.

As a result, hedge funds were carrying huge losses. The losses for one hedge fund in particular, Melvin Capital, were so dramatic that billionaire investors had to step in with a $2.75 billion rescue package.

The Reddit Wall Street Bets board lit up with messages:

“It’s a class war [retail investors against Wall Street]. It’s time we fought back.”

And:

“[Hedge funds:] This is personal for me, and millions of others… I’m making this as painful as I can for you.”

And:

“There is and has been a ruling class whose sole purpose is to retain power. They gaslight us into thinking they know what is best for us. 1% knows better than 99%. This is not [about] stocks, this is a financial revolution…”

GameStop’s sudden rise and fall is a sign of the times.

We saw explosive mob anger in 2020 over social issues, political issues and health issues. Now we’re seeing it in the financial system.

The key driver informing retail investors’ decision to invest in GameStop wasn’t sound investment principles, it was misdirected anger.

The obvious theme here is that people are seriously angry. And it’s not going away. In fact, it’s building. Who knows how or when the next investment fad will emerge, pulling in retail investors and potentially causing more losses and more anger.

Maybe you’re hesitant about the historically high stock market valuations.

Or maybe you’re not just concerned about quickly changing sentiment for individual stocks, but quickly changing financial conditions in general…

The good news is: You’re still in control of your investments.

If you’re uncomfortable with the stock market, you can diversify into other assets. You have plenty of alternative options, a number of which we’ll cover below…

Confusion, today, is running rampant…

There’s confusion about the important role of speculation in financial markets. There’s confusion about hedge funds’ role in the financial system. And, as we already mentioned above, there’s lots of confusion about short selling.

What is the public’s idea of what constitutes a “speculator”?

A monocle-wearing, pinstripe suit-wearing billionaire sitting in a smoke-filled room, drinking $100 per shot Bourbon? Or, in other words, the Monopoly man — someone to be despised. Someone who performs no useful function in society, other than to enrich himself at the expense of the little guy.

Or is there more to being a speculator? What if they do actually provide a useful service?

To better understand speculation, consider this example…

Farmers have a difficult life. They toil all day — long before sunrise and long after sunset. They face uncertainties. What will the crop yield be this growing season? Will the weather ruin their harvests? How will the weather not only affect their crop, but the overall supply? And what about political factors, like a trade war that affects demand?

The farmer has to plant in the spring and worry about the price he’ll receive six months later, when market conditions may change.

Fortunately, the farmer can lock in his price — and mitigate some of his worries throughout the growing season. The farmer does so by entering the futures market and selling his crop (corn, wheat, soybeans, etc.) for delivery after the harvest.

The futures market

Futures are a contract that specifies a predetermined date and price for an underlying asset. There are futures contracts for commodities and financial instruments.

The farmer can only have price assurance at harvest time because of… a speculator. A speculator is on the other side of the futures contract.

Speculators will forecast the weather. They will consider the supply and demand fundamentals.

And they will take on risks.

The speculator could be correct, and if so, they can potentially make more money — the price specified in the futures contract could be lower than the current market price. But the speculator could also be wrong. That would happen if the current market price is higher than the futures contract price.

By entering the futures market, it could be a win-win for both the farmer and the speculator. The farmer gets to lock in a price, and the speculator has the opportunity to potentially make more money.

Clearly, speculators provide a useful service. They provide liquidity for markets. They provide stability for producers.

And speculators are involved in more than just commodities futures markets.

Hedge funds involved in financial markets are also speculators, yet in the public’s mind, they have long had a bad reputation…

To understand “Wall Street hedge funds,” you first need to have a better understanding of what Wall Street is and how it functions.

“Wall Street” is huge. It’s not some monolithic organization.

There are giant investment banks with trillions in capital. There are investment advisors who help clients build a diversified portfolio and navigate markets. And then there are hedge funds — even single-man and woman shops — that may manage billions or as little as $25 million or so for their clients.

When the US investment banks lose, they go hat-in-hand to Washington D.C. for a taxpayer-funded bailout.

But you can’t automatically lump in ALL hedge funds with crony investment banks. There are plenty of hedge funds that simply invest clients’ money… and are very successful in doing so.

And we’re not being naive and dismissing the rampant cronyism among some hedge funds. Some of these funds pay former Treasury and Fed officials hundreds of thousands in speaking fees — a prepayment for future influence. And some hedge funds even hire former Treasury and Fed officials as high-paid consultants for insider information.

Whether given to cronyism or not, hedge funds often have an investing edge over retail investors. That’s simply the structure, and a function of their access to far larger data sets and far more sophisticated data analysis capabilities.

Retail investors could not short GameStop in such a dubious way — by selling more shares of the company than were actually in existence. But hedge funds could… and did.

And when the price of GameStop shares was rapidly increasing and then suddenly halted, that’s when the Reddit users screamed “cronyism!” from the rafters.

There’s a popular “theory” regarding the actions of prominent fund manager Steve Cohen…

Cohen was an investor in Melvin Capital (the fund we mentioned earlier), so he was exposed to the GameStop losses. So, as the theory goes, he ordered Robinhood to halt trading for retail investors.

But, like radio broadcaster Paul Harvey would say, then there’s also the rest of the story…

Government regulations require that brokerages carry a certain amount of capital in relation to the amount of money in their brokerage accounts. This is referred to as the brokerage’s capital requirement.

If a brokerage firm has $100 million between all its accounts, the government’s capital requirement regulations could translate into, say, $100,000 of cash on-hand.

Of course, the brokerage firm could voluntarily exceed the capital requirements. For example, $200,000 of cash on-hand would cover customers’ $100 million and leave room for further capital appreciation.

But when GameStop instantly soared in price — and about half of Robinhood accounts held GameStop stock — then Robinhood could not meet its capital requirements. And that would have turned into a major problem for Robinhood.

So, already facing a shortfall in its capital requirements and with GameStop shares potentially going even higher, Robinhood temporarily halted trading. The firm borrowed $600 million. And investors injected $1 billion.

The infusion of cash allowed Robinhood to meet its capital requirements.

And then, Robinhood once again opened up trading.

But the damage was done.

The narrative of crony Wall Street hedge funds versus the little guy picked up steam. There was a rush — including by incompetent individuals — to explain what just transpired. Hedge funds were demonized, and as was short selling…

Amidst the flurry of reporting on GameStop, we saw some seriously flawed thoughts…

As we noted before, speculators — and the whole notion of speculating — were skewered. Even some leading publications were utterly confused…

For example, The New York Times incorrectly reported that Robinhood had to raise money so they could pay their account holders. That’s nonsense. A brokerage doesn’t pay a shareholder when they sell. Instead, it’s merely an intermediary to facilitate buying and selling between investors.

It’s clear that some of these journalists have no understanding of how the stock market works.

And unsurprisingly, the press — including some in the financial press — got the definition of short selling wrong…

Some chimed in that there was an expiration date for selling short, as if one was dealing with options. Others commented in general that short selling offers no value.

The key take-out here is that you cannot rely on the financial press for your financial education. There are, however, time-tested resources that can help you develop a sound investment perspective. We discuss some of our favourite books on this topic below…

When financial conditions change, even some advisors can get caught off guard

In the 1960s, the “Nifty Fifty” stocks were all the rage.

The Nifty Fifty consisted of large capitalization stocks that seemed invincible at the time. There were companies like Dow Chemical and McDonald’s, which are still today in the Dow Jones Industrial Average — the top 30 companies by market cap.

But there were also some companies like Polaroid and Eastman Kodak, which today are shadows of their former selves.

Back in the 1960s, the Nifty Fifty were considered the “easy button” of investing. Just buy these stocks, sit back, and watch your net worth grow.

And the Nifty Fifty performed well — until financial conditions changed, that is.

Then, individual stock pickers had an advantage over those pushing the easy button.

Today’s “easy button” is passive index investing. The strategy is to… just buy the index, sit back and watch your net worth grow.

But what if financial conditions were to change suddenly?

There are financial advisors out there who, in 2020, experienced their first recession as professionals. Before the shock of 2020, two things were certain for this group: 1) Interest rates were falling, and 2) Stock prices were climbing.

And even older financial advisors haven’t experienced dramatically different financial conditions that last long term, like the double-digit inflation days of the early 1980s.

Only those aged around 60 years old or older would have dealt with roaring inflation during their investment careers.

Forty years of deflation has lulled many investors and advisors to sleep…

And some may not wake up in time to see what’s happening…

The Federal Reserve is targeting an annual inflation rate of 2%. And Fed officials assume that we’ll get there in a steady, linear progression — a “Goldilocks” step-up to their neat, tidy inflation target. Meaning: No major economic shocks. No rapidly accelerating inflation. Instead, by their wise guidance and lever-pulling, we’ll have an economy that’s just right.

That may be a fantasy. The US inflation rate could blow past 2% and then climb to 5%.

And the assets that perform well in a deflationary environment won’t be the winners in an inflationary period. In fact, if inflation starts to run hot — higher than, again, the Fed’s annual 2% target rate — then as bond yields rise, bond prices would fall substantially. (Bond yields and prices move inversely.)

Also, while inflation rises, investors can also get hit with falling stock prices.

Sure, there are consumer staple companies (e.g. Walmart or Dollar General) that might fare fine during times of inflation. The same goes for companies well suited to our digital age (e.g. Amazon).

The same could be true for natural resource companies. And those with a strategic advantage. And particularly companies that transport natural resources with a built-in strategic advantage (e.g. BNSF Railway — which now doesn’t have to compete with the Keystone Pipeline to move oil across North America).

(Please note that this is NOT a recommendation of Walmart, Dollar General, Amazon or BNSF stock. Instead, these are mentioned for illustrative purposes only.)

The point is… your current investment portfolio might not be well suited for (quickly) changing financial conditions. That’s why it’s important to consider diversifying beyond just traditional financial assets like stocks and bonds in your home country.

The asset classes discussed below are some alternative options to consider…

Download Our Free Perfect Plan B Guide

Download our free Perfect Plan B Guide and learn no-brainer strategies on how to legally reduce your taxes including…

You’ll also learn many other useful strategies such as how to generate strong investment returns while taking minimal risk, and how to obtain a valuable second passport.

Most likely, you, as an individual investor, cannot beat the hedge funds.

You don’t have the resources. You don’t have the computing power. You don’t have the capital.

But none of that matters if you take a different approach.

You’re only limited by the amount of work you’re willing to put in and your patience.

You have some incredible investing advantages: You don’t have to manage other people’s money. In other words, you won’t face angry investors looking to pull money out of your fund.

And you can go where large financial institutions cannot.

Hedge funds and banks need to invest in large market cap companies. They’re not nimble enough to invest in small market cap companies with growth potential. These institutions would move the market price far too much. But that doesn’t apply to you.

Or, you can choose an entirely different direction — foreign stocks, emerging or even frontier market bonds, foreign cash flow generating real estate, precious metals, royalties, cryptocurrencies or even private businesses.

We’ll cover each of these categories below…

Before risking capital, start by investing in your financial education first

Whether you’re adding skills to get that promotion at work or to build your business, you can never go wrong by investing in yourself.

The same principle applies for investing.

No one automatically knows how to be a good investor. Instead, investing is a skill. It takes time, resources and often mistakes (that are hopefully not too costly).

To help reframe your thinking about assets, liabilities, cash flow, and to develop a disciplined approach to your finances, you can read classics like:

And for a deeper dive into investing, you can also read:

We’re writing to educate and to inform, NOT to advise or recommend

We’ve noted this before, but we want to emphasize it again…

We’re not investment advisors. We’re covering the asset classes below for educational and informational purposes only.

At the very least, after reading this article, you’ll know a little more about these asset classes. And if you want to take action, you can be more confident and informed when you speak to your financial advisor.

To best illustrate the deal you can get on value stocks, here’s a thought experiment…

Let’s imagine that I have a business.

My business is worth $1 million, which includes $100,000 in cash. The other assets are valued at $900,000. And I’m very disciplined, so there’s no debt.

What if I wanted to sell that business… and I offered it to you for only $75,000?

How fast would you take that deal? In fact, you’d be crazy not to take it.

You could get the company’s assets for free, AND instantly put $25,000 ($100,000 in company cash less the $75,000 buying price) in your pocket.

There’s no way that this deal would happen with a private business sale. The owner would take the $100,000 cash and sell the business at some multiple of sales, earnings or levered free cash flow.

(Earnings — also known as profit or net income — can easily mask a company’s true financial position, because of accounting rules. But “levered free cash flow” is a better representation of the company’s health. This is the amount of operating cash flow after a company pays its financial obligations and reinvests into the core business.)

But in publicly-traded markets, these kinds of deals are possible.

Yes — it’s possible to buy stocks that are trading for less than net cash.

To be clear, “less than net cash” means that the company’s market capitalization is less than the company’s cash on its balance sheet (minus ALL debt). If I were crazy enough to sell my private business to you in the example above, you could buy my company at a 25% discount to net cash.

So, why do these less than net cash opportunities exist in publicly traded markets?

Because of a couple reasons.

First, compared to financial markets in the US, Canada and Europe, there are far fewer eyes on stock markets throughout Asia and Africa — where you find these value opportunities. Investment banks will have dedicated analysts to cover and know all the details about large cap US stocks. But these resources are not devoted to many foreign markets.

Second (and related to number one), individual investors often overlook foreign value opportunities. Investors often fall prey to “home country bias” — most or all of their investments are in their home country. There’s a lot of emotion wrapped up in investing. So, the fear of the unknown keeps investors from exploring great deals around the world.

Foreign value stocks are definitely not risk-free…

There’s always the risk that you can invest in “value traps” — stocks that never appreciate in value and trap your capital. In that case, there’s an opportunity cost involved.

And at the moment, value investing is out of vogue. People are busy chasing high-flying tech stocks. When the stock price rises, greed takes over and they rush in to buy more.

But at some point, fear will replace greed. (We cannot pretend to know when that will happen.)

And when emotions change, that capital flow into overvalued stocks could suddenly change. Those who bought at sky-high valuations could be left with huge losses. The panic selling will start, triggering more panic, causing more panic selling… and so on.

A potential result: Value stocks may shine once again.

You might want to consider diversifying a portion of your portfolio into value stocks. You can start with this free video presentation, which provides more details.

A metric that can help you define value

Just because a company is trading for less than net cash doesn’t automatically mean that it’s a good buy. You need to consider the health of the business, the quality of the management, the industry’s mid-term prospects, and other factors.

So, it’s not always possible to find promising opportunities for less than net cash.

As an alternative, you could also consider other value companies. These may not be trading for less than net cash, but you can still get a great buy.

Tim Staermose, Sovereign Man’s Chief Investment Strategist, uses a metric to define value:

(ROE/(P/B)) > 15%

That is, the Return on Equity divided by the company’s Price to Book ratio must be greater than 15% per annum.

Return on Equity reveals the company’s profit for each dollar of capital deployed in the business. And Price to Book compares a company’s market cap to its book value — the company’s total assets less intangible assets (patents and goodwill) and liabilities.

A stock with a 30% ROE for example, if trading below 2x book value, would be a screaming buy, as long as all other things checked out — starting with low or no debt on the balance sheet, and whether the company has an ethical and competent management team whose interests are aligned with those of minority shareholders.

In June 2017, Argentina sold $2.75 billion worth of bonds.

That’s not incredibly remarkable. To finance operations, governments around the world sell bonds every single day of the year.

What was remarkable was the duration of these particular bonds…

A bond is similar to a loan; as an investor, you’re basically loaning money to whichever government issues the bond. And, like a loan, a bond has a maturity date — the date at which the government is supposed to pay you back the “face value” of the bond.

Car loans often have a three to seven year term. Student loans can easily have 10 to 15 year terms, while a home mortgage in the US can last up to 30 years.

It’s the same with government bonds, which often have a term up to 30 years.

Needless to say, the longer the term, the riskier the bond. Plenty of things can go wrong if you give governments enough time to screw up.

So take a guess when Argentina’s bonds were set to mature — 10 years? 30 years? 50 years?

Try 100 years. An entire century.

And the 100-year bond carried an enticing 7.125% annual yield. Investors, desperate to obtain yield in a low interest rate environment around the world, rushed in. Argentina received $10 billion in bids for that $2.75 billion of 100-year bonds.

Clearly, investors ignored the risks. Since Argentina’s independence in 1816, the country had defaulted on its debt nine times.

Unsurprisingly, just three years after issuing these 100-year bonds, Argentina was forced to restructure its debt. Over the three years, the value of the 100-year bonds had dropped 56.75%.

In other words, investors who held the bonds recovered only 43.25 cents on the dollar.

This was another tough lesson for those investors who ignored the risks.

But not all emerging or even frontier market bonds are fraught with such risk as those issued by Argentina.

In fact, there are countries with far more favorable demographics — a higher percentage of young people, which signals growth potential — and, even in the wake of COVID-19, higher tax receipts, another sign of a growing economy.

The frontier market of Tanzania is such an example. By 2040, Africa is projected to have one billion workers — more than China and India combined. (Yes, we realize that there is no one “Africa” and don’t want to generalize.)

Aside from favorable demographics, the Tanzanian President did not close the economy due to COVID-19. So, without business restrictions and rising defaults, banks are not suffering. And government tax revenues rose more than 20%, year on year, during each month of 2020.

With plenty of cash flowing into the Tanzanian government’s coffers, it is in a position to reward bond investors. Inflation is running at about 3% per year, so you can enjoy a 12% real rate of return on government bonds.

However, if Tanzania is a little too frontier for your tastes, you can stick with emerging markets.

There’s actually no agreed-upon definition of an “emerging market” country.

Morgan Stanley publishes a list of countries that it deems “emerging markets.” (The latest list includes: Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Kuwait, Korea, Malaysia, Mexico, Pakistan, Peru, The Philippines, Poland, Qatar, Russia, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey and the United Arab Emirates.

Click here for the performance of this index through January 2021.)

Of these countries, Indonesia, Pakistan and The Philippines all have younger populations, similar to Tanzania. So, you could consider investing in bonds in these countries if you’re more risk averse.

And Jim Rogers, legendary investor and friend of Sovereign Man, recently said that he’s bullish on Russia. He cited two reasons: One, because it’s undervalued. And two, the country has a lot of oil and agricultural commodities, which he’s also bullish on in 2021 and for the coming years.

Regardless of where you’re considering, again, there’s the default risk of corporations and governments. Carefully weigh those risks before investing.

And there is also foreign currency risk — both for the local currency and the US dollar.

Companies in emerging market economies will often borrow in dollars. Meanwhile, these companies generate revenue in the local currency.

So, if the USD weakens against the local currency, all else being equal, foreign companies’ margins will automatically increase.

But if the USD strengthens, these companies face higher financing costs and, again all else being equal, margins will automatically decrease.

Be sure to consider these risks in emerging or frontier markets carefully. If bonds in these countries are not appealing to you, then there are always real foreign assets to invest in…

By itself, foreign, cash flowing real estate can provide a lot of value.

Imagine having an apartment in Madrid. Or a house in the Algarve region of southern Portugal, right on the water.

But beyond just diversifying internationally into a real asset, an investment in foreign property can also provide another major benefit…

A built-in Plan B.

By purchasing real estate overseas — typically at a government specified price point — you can secure a foreign residency in a number of countries. That way, you can expand your options beyond your home country, especially in this post-COVID era full of travel restrictions and lockdowns.

Several European countries offer “Golden Visas.”

Bulgaria, Greece, Ireland, Latvia, Malta, Portugal, Spain and the United Kingdom all have some version of a Golden Visa.

To be clear, a Golden Visa is NOT a Citizenship By Investment Program. Rather, it is a residency… that can usually also lead to eventual citizenship.

And in most cases, you only need to vacation in the country for a few days per year to maintain your temporary residency and then to qualify for permanent residency. (One notable exception is Latvia. You need to commit to living in Latvia for four out of the five years of your initial residency.)

But spending time in beautiful, sunny places like Portugal or Spain is hardly a hardship.

Foreign real estate is a great way to knock out two birds with one stone. If you have the means, and your goal is to live in Europe — plus you don’t need a European passport right away — then you may want to consider one of these programs.

(A reminder to Sovereign Confidential subscribers: In late 2020, we updated our European Golden Visas Black Paper. Sign into the members site to see if one of these programs is right for you.)

In the past 200 years, over 650 paper (fiat) currencies have been cancelled, replaced, or inflated away.

But precious metals have withstood the test of time. In fact, over the past 5,000 years, gold and silver have retained their value.

Let’s be very clear: Physical gold and silver are not an investment…

Rather, physical precious metals are an asset. Think of these metals as an “anti-currency”.

By holding a portion of your wealth in physical gold and silver, you’re making a conscious decision, or giving precious metals a vote of confidence. You’re effectively saying, “I choose to preserve some of my purchasing power in physical gold and silver. I’m not placing my full faith in fiat currencies, which can be eliminated… along with my hard work and savings.”

When central banks around the world are printing so much money and governments are immediately spending it, you might want to consider holding physical gold and silver to preserve your buying power long term.

To discover more about silver, you can reference our in-depth silver article published in early 2021. And for even more information on gold and silver, click here to get our Free Ultimate Gold and Silver Guide.

Again, physical precious metals are an asset, not an investment. But there are ways to invest in precious metals…

Know that just as with any other investment, there can be significant downside risks.

Precious metals investment opportunities include:

In our Ultimate Gold and Silver Guide, we discuss these investment options and much more. You can download that guide for free to consider the options that might be best for you.

A royalty is a payment for the ongoing use of an asset.

In the precious metals section above, we mentioned that a royalty company is a way to invest in precious metals. You can also own mineral rights and receive an ongoing royalty payment from an oil and gas company that has producing wells.

But royalties are not limited to natural resources.

Creators and performers of songs, movies and television shows own royalties from their assets or intellectual property (IP).

A song royalty, for example, is a REAL asset that produces income, just like agricultural property or a profitable private business. Royalties give you collateral… that may have consistently generated thousands or even millions of dollars in income and will continue to do so.

None other than Warren Buffett — one of the greatest, if not THE greatest investor of all time — compared a royalty to owning a tollbooth.

Once you make the initial investment, your upkeep is minimal.

But you collect cash into perpetuity as cars pass through.

Until recently, unless you personally wrote or performed a song, for example, it was difficult to buy the royalties for that song. The same goes for royalties on movies, television, book publishing, etc.

Fortunately, today there is a growing market to buy and exchange royalties.

Royalty Exchange is one such an online marketplace.

(Full disclosure: The previous CEO of Royalty Exchange is a good friend of Simon Black, Sovereign Man’s founder. But neither Simon nor any Sovereign Man employee receives any commissions or fees from Royalty Exchange. Also, Sovereign Man’s Total Access members — our highest-level membership — had an opportunity to invest in one of Royalty Exchange’s previous financing rounds. We’re mentioning Royalty Exchange for informational purposes only. Before purchasing a royalty, you should complete your own due diligence and consult with a financial advisor.)

A claim on a high-quality, established song, television show or movie royalty can be extremely valuable. Again, using the example of a song, you can collect income from artists who want to record a cover. And you don’t need a legion of workers to grow your income.

However, you should note that there are risks associated with royalties.

There are still things out of your control, like consumer tastes changing. And, with countless concerts and shows having been cancelled in 2020, royalty owners counting on public performance income were left sorely disappointed.

Still, if you buy the right royalty, you can own an asset that’s largely uncorrelated to financial markets. (“Uncorrelated to financial markets” means that there’s little to no relationship with the performance of stocks and bonds.)

And in today’s ultra-low interest rate environment, you can have a stream of income that generates potentially double-digit annual returns.

Speaking of large annual returns…

Since emerging in 2009, cryptocurrencies and blockchain technology have started to turn the global financial and banking system on its head.

This technology completely decentralizes the financial system.

Banks no longer get to hold everything hostage on balance sheets and ledgers that they control.

And the blockchain can revolutionize more than just finance. Real estate property records, insurance records, and basically anything that’s centralized in a database is primed for disruption.

Over the next few years, as more companies develop innovative blockchain solutions, we’ll see more industries being disrupted.

We’ve already seen cryptocurrencies like Bitcoin gain more traction, especially over the last year or so. As we write this report, Bitcoin’s market cap has exceeded $1 trillion.

And cryptocurrencies are enjoying far wider adoption than merely among individual investors.

In August 2020, instead of only holding US Treasury notes and bonds, software company MicroStrategy put $500 million into Bitcoin. MicroStrategy was the first publicly traded company to hold Bitcoin on its balance sheet.

But MicroStrategy won’t be alone…

In February 2021, electric car manufacturer Tesla announced that it’s buying $1.5 billion in Bitcoin to hold as a cash reserve. Other companies and institutional investors are expressing interest in diversifying into cryptocurrencies, too.

Despite all this interest, cryptocurrencies are not an investment. They’re a speculation.

(Importantly, an investment can be defined as an asset that pays you to own it. Cash flow generating real estate or a high-quality, dividend-paying stock are both examples of investments. But if the only way to make money on your asset is to sell it at a higher price, then your asset is not investment. Rather, it’s a speculation.)

With a supply of only 21 million Bitcoin, if demand continues to increase, Bitcoin’s price would further appreciate.

But there’s also the chance that demand craters, in which case Bitcoin’s price would then fall. (Demand could crater because capital leaves cryptos for another asset. Or if the government threatens a crackdown on crypto assets, holders may get worried and sell.)

Please note that Sovereign Man is not recommending buying Bitcoin or any other crypto asset. This article should be treated as general information on the topic only.

Buying cryptos could be a way to diversify your portfolio… but only once you’ve considered the risks and spoken to a qualified financial advisor.

Finally, there’s another asset class that can offer suitable portfolio diversification…

“Hello Apple headquarters…”

“I’d like to speak to Mr. Tim Cook [the CEO of Apple]. I’m an Apple investor, and I have a few ideas that I’d like to run by Mr. Cook to improve the business. Can you please connect me?”

The beep of your cell phone.

That’s likely what you would hear. Because your conversation would end.

Unless you own 10% or more of Apple stock (worth over $200 billion at the moment), then Tim Cook will not be taking your call. And if you show up in-person to Apple headquarters in Cupertino, CA and demand a meeting, then security will quickly escort you out of the building.

But the CEO of a private business can — and should — pick up the phone or meet in-person with his or her investors.

One of the great benefits of investing in private businesses is having access to senior management. Sovereign Man likes to regularly check in with the management of private businesses that we invest in. This enables him to gauge how well they’re executing on their stated business strategy, and to ensure that they’re executing as promised.

Private investments are an asset class that’s popular with accredited investors. (But anyone can invest in a private business, like loaning your neighbor some money to grow his cafe business.)

Early-stage investors can get better valuations than individuals investing in publicly traded stocks.

You have the opportunity to own a significant portion of the business, giving you potentially large growth and a favorable exit opportunity down the road.

PLEASE NOTE: Early stage investments carry a significant amount of risk — you could lose all capital invested in a startup business. It is therefore vital that you do thorough due diligence before making such investments, and be sure to discuss this with a financial advisor familiar with your unique situation.

We don’t know exactly when the overvalued stock market may take a sudden plunge.

Maybe we have a few more years until a big crash. Or maybe it happens later in 2021.

But you don’t have to wait for a correction and be fully exposed to the carnage. You don’t have to blindly follow the crowd and the coverage in the financial media.

Instead, first recognize that you’re still in control of your investment choices.

Once you’ve acknowledged that fact, then take some time to educate yourself on other, unconventional investment options.

That was our goal with this report. Use the information we presented as a springboard for your own research, and be sure to download the free resources mentioned throughout the report.

And remember: Just as with US stocks, investing outside the mainstream certainly has potential risks.

But it’s also possible to find outsized returns in foreign value stocks, emerging or frontier market bonds, foreign real estate, precious metals, royalties, cryptocurrencies and private businesses.

Your investing future is in your hands.

No one else cares more about your money than you. So, we encourage you to conduct thorough due diligence on opportunities across these various asset classes before making any investment decisions.

Consider the risks, your goals, and your preferred investment timelines… And then confidently speak to your financial advisor, knowing that you’re informed regarding many of the opportunities out there.

Learn EVERYTHING you need to know about

buying, owning, storing and investing in gold & silver…

Download our FREE precious metals report and learn…

Legal Disclaimer:

Neither this document, nor any content presented by our organization, is intended to provide personal tax or financial advice. This information is intended to be used and must be used for information purposes only.

We are not investment or tax advisors, and this should not be considered advice. It is very important to do your own analysis before making any investment or employing any tax strategy. You should consider your own personal circumstances and speak with professional advisors before making any investment.

The information contained in this report is based on our own research, opinions, as well as representations made by company management. We believe the information presented in this report to be true and accurate at the time of publication but do not guarantee the accuracy of every statement, nor guarantee that the information will not change in the future.

It is important that you independently research any information that you wish to rely upon, whether for the purpose of making an investment or tax decision, or otherwise.

No content on the website (SovereignMan.com) or related sites, nor any content in this email, report, or related content, constitutes, nor should be understood as constituting, a recommendation to enter into any securities transactions or to engage in any of the investment strategies presented here, nor an offer of securities.

Sovereign Man employees, officers, and directors may participate in any investment described in this content when legally permissible, and do so on the same investment terms as subscribers. Sovereign Man employees, officers, or directors receive NO financial compensation from companies who appear in this report.

Join over 100,000 subscribers who receive our free Notes From the Field newsletter

where you’ll get real boots on the ground intelligence as we travel the world and seek out the best opportunities for our readers.

It’s free, it’s packed with information, and best of all, it’s short… there’s no verbose pontification here– we both have better things to do with our time.

And while I appreciate all the visitors who stop by our website, I provide special bonuses to our email subscribers… including free premium intelligence reports and other valuable content that I only share with them.

It’s definitely worth your while to sign-up, and if you don’t like it, you can unsubscribe at any time.

How did you like this article?

Click one of the stars to add your vote...

Other readers gave this article an average rating of 5 stars.