US National Debt:

Shocking Facts & How You Can Protect Yourself

-

AUTHOR

James Hickman -

PUBLISHED

June 29, 2018

What if I told you that by the time you finished reading this sentence, the US national debt would have shot up by $364,000?

Or – that by the time you wake up tomorrow, the debt will have increased by nearly $1.5 BILLION?

Or – that in just a split second the US national debt increases by more than the typical American earns over the course of an entire year?

These are not exaggerations. They are real numbers, pulled from the government’s own public ledgers and projections.

And the national debt currently stands at…

Over $21 TRILLION

Current US National Debt

That’s a number with TWELVE zeros.

A “trillion” almost seems like a fantasy… a made-up number like “a bajillion” or “zillion”.

It’s a number so large that our minds don’t even have the ability to grasp the real meaning of it, because there is so little within our physical human experience that we can relate to it.

To put the number into perspective, consider that in the entire history of humanity no other nation has ever had as much debt as the United States. And yes, that fact is adjusted for inflation.

But most importantly, no nation (or even empire) in the entire history of humanity has ever survived carrying a large national debt over the long-term.

It would be foolish to assume that there will be no consequences to the unsustainable national debt.

Eventually the US will share the same fate as all other heavily indebted nations and empires: An initial erosion of its citizens’ wealth through inflation and an eventual financial collapse.

That’s why this article will not only answer your burning questions about the US national debt, but it will also show you how you can protect yourself from these consequences.

In fact, this article will show you how you can put yourself into a position of strength and actually benefit from the debt situation. Because whenever there is turmoil, there is also extraordinary opportunity.

Once the music stops playing, there will be many losers. But there will also be a few who had the foresight to prepare and create wealth that will last for generations.

My goal with this article is to help you end up on the winning side of history.

How To Protect Yourself AND Benefit

From The US National Debt

The national debt is a problem. Not just for the US, but also for you personally, because as you’ll learn in this article… Ultimately it is YOU who is on the hook for it.

Download our most actionable quick-start guide full of…

No-Brainer Strategies to Ensure You Thrive No Matter What Happens Next

Learn about these and many more strategies in our free Perfect Plan B Guide.

They will ensure you are in a position of strength and won’t just survive the inevitable consequences of the US national debt, but will actually benefit and thrive from them.

If you have trouble envisioning $21,000,000,000,000, that’s understandable.

Here’s a reference that should help:

Picture a regulation-size American football field. With the end zones, the field is 120 yards long and 53.33 yards wide.

Now, imagine that $100 bills cover EVERY SQUARE INCH of this football field.

Got it?

Next, add layer and layer of $100 bills until you have the Benjamins stacked in 10-foot high piles. The top of these piles will be even with the goal post crossbars.

To reach $21 trillion, you’d need 10-foot high money piles of $100 bills on…

14.5 football fields!

That means the fields of nearly half the National Football League’s 32 teams would be piled high with $100 bills!

Need another reference? How about a time perspective of so much money?

Let’s say you start spending money when Jesus was born. The first Christmas.

You start spending $1,000,000 every hour. Over two thousand years pass, and by a miracle, you’re still alive… and you’re still spending $1,000,000 every hour since Jesus’ birth.

So, spending $1,000,000 X 24 hours per day X 365 days per year X 2018 years…

You’d spend $18 trillion. You’d still be short of the US national debt.

If you spent $1,000,000 every hour for 2,000 years…

You’d STILL spend only $18 trillion. You’d still be short of the US national debt by $3 trillion.

Let’s put it a different way:

The US national debt is 105% of Gross Domestic Product (GDP) - the value of a country’s total goods and services.

That means the debt is bigger (by 5%) than the entirety of what America earns as a whole.

Bigger than the entire US economy.

(By comparison the national debt was just 31% of GDP in 1981, not even a full third of the US economy.)

Worse, the Treasury Department has already estimated that it will borrow $1 trillion this fiscal year, $1 trillion next year, and another trillion dollars the year after that.

Can you see the insanity?

But The Scariest Factor Is...

How Quickly The US National Debt is GROWING

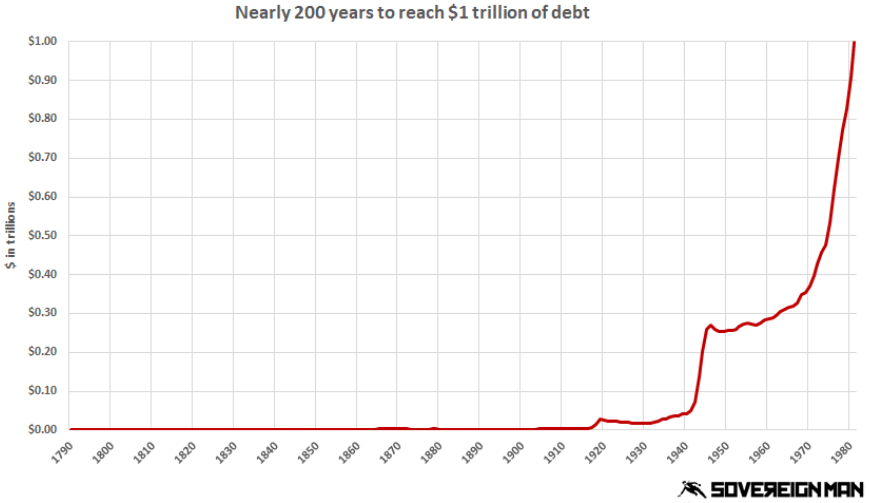

On October 22, 1981, the national debt in the United States crossed the $1 trillion threshold for the first time in history.

People were rightly dismayed. It had taken nearly two centuries to reach that unfortunate milestone.

And over that time the country had been through a revolution, civil war, two world wars, the Great Depression, the nuclear arms race… plus dozens of other wars, financial panics, and economic crises.

Today’s $21 trillion was hit recently.

Were you born in the late 1970s or early 1980s? Well, then it’s just over your lifetime that the government has added that extra $20 trillion to the national debt.

So, it took 200 years to reach the first trillion… and about 40 years to reach the next $20 trillion.

Again, that’s an average, over those four decades, of nearly $1.5 BILLION added to the national debt every single day…

$62 million per hour…

$1 million per minute…

and more than $17,000 per SECOND are added to the US National Debt every single day…

And there is no end in sight.

How do you like this article?

Click one of the stars to add your vote...

Other readers gave this article an average rating of 4.9 stars.

In this section you’ll learn why the Chinese-owned debt is not what you should be worried about...

In a nutshell, YOU are the biggest owner…

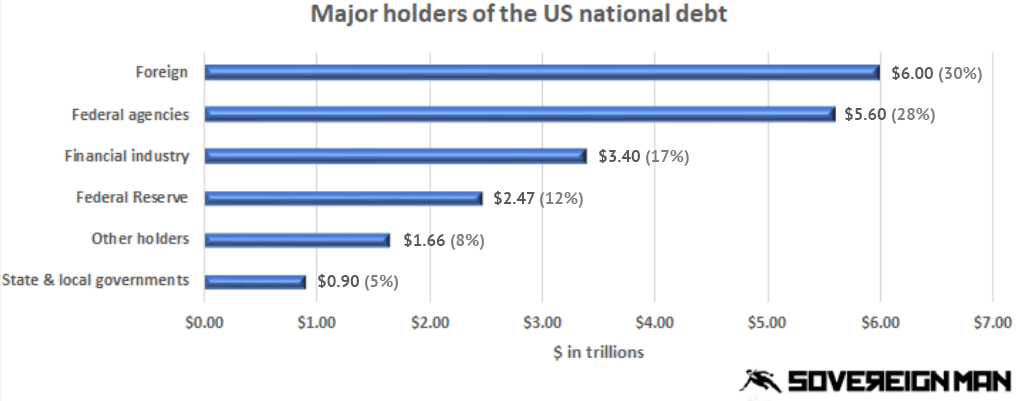

If you are like most people, you probably have the most concerns about the Chinese and other foreign holders of the national debt. But in reality you should be most worried about the national debt owned by the American people…

It’s bigger than all the foreign holders combined.

This may seem unbelievable at first… after all, you personally may not even own any national debt, but hear us out…

Let’s take it step-by-step and in a moment it will all make sense. We’ll start with the biggest holders of the national debt…

Based on various financial reports from the United States Government

1. Foreign Holders

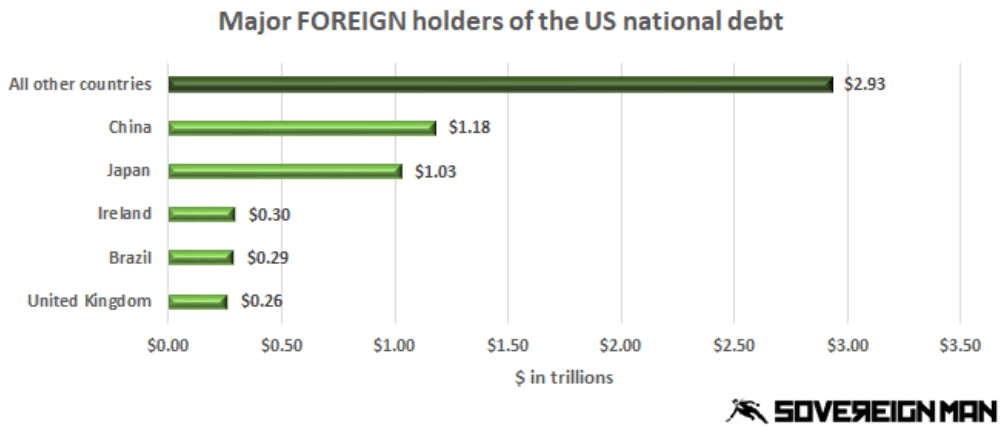

At $6 trillion and 30% of the total debt, foreign holders own the biggest chunk of the US national debt.

The Chinese lead the way closely followed by the Japanese at over $1 trillion each. Ireland, Brazil and the United Kingdom round out the top five foreign debt holders.

But the majority of the foreign holders are all the other countries that own a smaller piece of the debt.

2. Federal Agencies

The second biggest holder are other branches of the US government. You may feel relieved reading this… after all, it looks like the US government owes a huge portion of its debt to itself and could simply “erase” it if it wanted to…

But it’s important to look closer, because this is the first way of how you own a big portion of the government debt.

The vast majority of this debt is actually held by various government funds such as Social Security and retirement funds.

The US government has made the promise to take care of its citizens. To achieve this goal they put a portion of the collected tax revenue into various funds.

These funds don’t just keep the money in the bank and instead invest a portion of it into various financial instruments to grow it. One of these financial instruments is the national debt in the form of government bonds.

But the important thing to realize here is that this money belongs to the American citizens and not to the government.

And the government has the obligation to pay back that debt in order to allow the Social Security Trust Fund and other funds to fulfill their obligations to the people.

If they don’t pay it back, then it is you, the American citizen, who is on the hook for that debt.

3. Financial Industry

The third biggest holder is the financial industry. These are mutual funds, banks, private pensions, insurance companies, savings bonds and so on.

This is another way of you how are exposed to and own the government debt. Even if you personally don’t own the debt, you certainly have a bank account, a 401(k) or an IRA.

And these financial institutions own government bonds purchased with your money.

4. The Federal Reserve – America’s central bank

The Federal Reserve is the fourth biggest holder. It’s the central bank of the United States and also known as “The Fed”. And although it sounds like a government entity, there is nothing “federal” about the Federal Reserve– it’s a private institution.

This private institution has control over the money supply of the United States. It establishes interest rates and has the power to conjure money out of thin air.

This is extraordinary power. And it has been awarded to an unelected committee of power brokers – many who come from the investment banks.

It works like this:

The Fed literally creates money out of thin air and buys government debt with it. The government uses that money to fund government operations, but in return it has to pay interest to the Fed.

Then the Fed pays out a portion of the earned interest and other profits as dividends to its shareholders… who happen to be other private banks such as JPMorgan.

Much of your income taxes are not used for roads, schools or other public services, but are spent on interest paid to the Fed… on money it created out of nothing.

It’s a perverse system designed to transfer wealth from the American people directly to the banking elite. By continuing its unsustainable spending and debt habits, the US government is stealing from the future – your future and your children’s future.

5. Other holders

Other debt holders include individuals, bank trusts and estates, businesses and other investors… to the tune of over $1.6 trillion.

Included among these “other holders” of US debt is legendary investor and CEO/chairman of Berkshire Hathaway, Warren Buffett. Berkshire has over $100 billion parked in short-term Treasury bills.

6. State & Local Governments

Large financial institutions, hedge funds and other investors are not alone in their holdings of US government debt.

Your state government has money invested in US government debt. And it’s likely that your local government also holds federal debt.

So, with your state and even local government holding a portion of the US national debt, you’re a creditor exposed in multiple ways to a federal government default.

Why Ultimately You Are on the Hook for the Debt

The Social Security “Trust Fund” owns $2.8 trillion… roughly the same as the top 5 foreign holders of US debt.

Medicare owns another $294 billion.

Financial institutions own $3.4 trillion.

That’s a total of about $6.5 trillion and about one-sixth of the national debt. This is an even larger amount than all the foreign holders combined and makes YOU the largest holder of US national debt.

Whether you like it or not… Your money is exposed to the national debt and you are a holder of the US national debt in one form or another.

Nobody knows exactly when, but at some point, this whole debt bubble will pop.

This pop will be a government default on its debt, and based on other government defaults throughout history, the situation won’t be pretty.

But congratulations: You’re on the hook for this massive, unsustainable debt. You’re left holding the bag. You and your family are the ones who will fight for a chair when the music stops.

FREE GUIDE

How To Protect Yourself AND Benefit From The US National Debt

As you can see, the national debt is a problem. Not just for the US, but also for you personally, because ultimately it is YOU who is on the hook for it.

Download our most actionable quick-start guide full of…

No-Brainer Strategies to Ensure You Thrive No Matter What Happens Next

Learn about these and many more strategies in our free Perfect Plan B Guide.

They will ensure you are in a position of strength and won’t just survive the inevitable consequences of the US national debt, but will actually benefit and thrive from them.

Many government debt apologist try to downplay the debt... But in this section you'll learn why they are wrong and why the national debt is a big problem.

You’ll find all sorts of articles out there that tell you to forget about the debt.

Don’t worry – you don’t understand the big picture, some of these people may say. They may reach into their bag of quotes and pull out one like, “Only small minds are impressed by large numbers”, from Arthur Clarke.

Or, they’ll exclaim that obsessing about such a trivial number as $21 trillion is just hysteria.

I totally disagree with this premise and here are the facts to prove why these excuses are wrong.

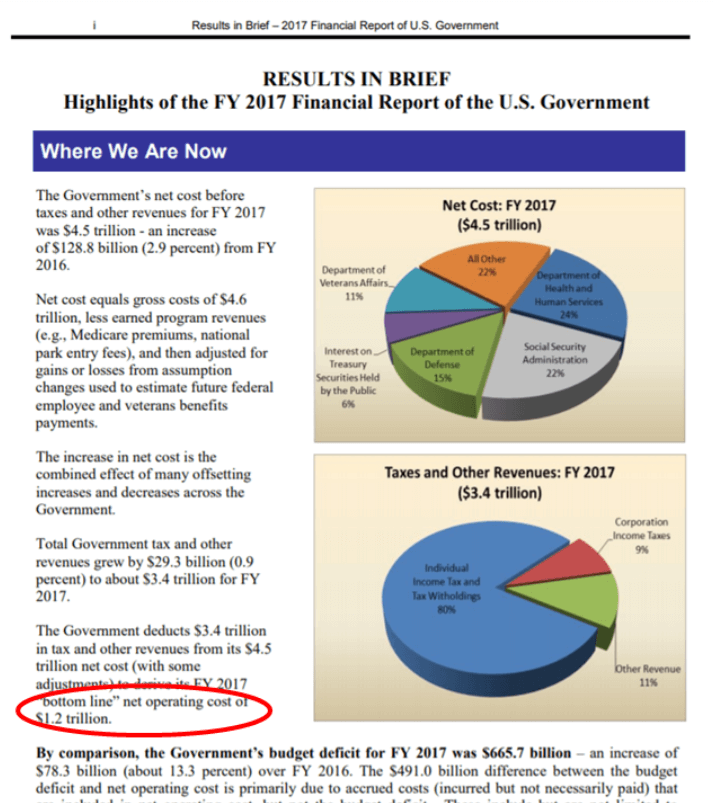

In early 2018, the United States government released its annual financial report for the previous year.

This is something the government does every year, similar to how large companies like Apple, or Warren Buffett’s Berkshire Hathaway, publish their own annual reports.

Unlike Berkshire and Apple, though, whose financial reports typically show strong, positive results, the US government’s financial statements are a complete horror show.

Right at the beginning of the report, the government explains that its “net loss” for the year was an unbelievable $1.2 trillion.

That’s simply staggering.

The US government’s loss in 2017 is larger than the entire Australian economy.

This is not a conspiracy theory or irrational fantasy.

This is the Treasury Secretary of the United States of America publicly announcing that the federal government lost $1.2 trillion.

What’s even more alarming is that 2017 was a great year.

There was no war. No recession. No epic financial crisis. In short, everything was awesome in 2017.

Even the government’s overall revenue was a record high $3.3 trillion for the year.

Yet despite all that good news… despite all those positive developments and record revenue… they STILL managed to lose $1.2 trillion.

If the government loses $1.2 trillion in a GOOD year, how much do you think they’ll lose in a BAD year? How much will they lose when they actually do have a recession to fight? Or another war? Or a major banking crisis?

More importantly, how long can something so unsustainable possibly last?

But the fun doesn’t stop here.

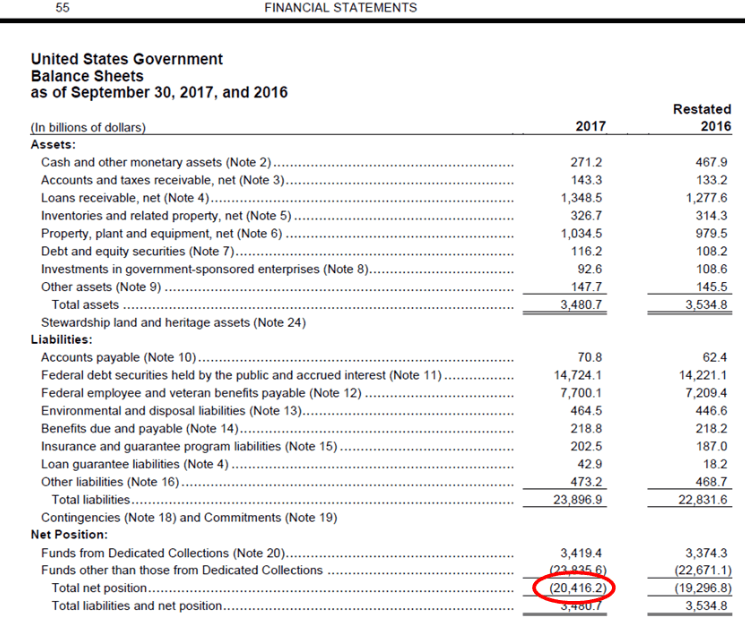

Further in the report, the government reviews its own assets and liabilities… effectively calculating its “net worth”.

It’s just like how an individual might calculate his/her own net worth – you add up the value of your assets, like your home, car and bank account balances. Then subtract liabilities like mortgage and credit card debt.

The end result is your net worth. And hopefully it’s positive.

The government’s net worth is hopelessly negative: MINUS $20.4 trillion.

And that’s worse than its result from the previous year’s MINUS $19.3 trillion – meaning that the government’s net worth decreased by about 6% year over year.

To be clear, a net worth of negative $20.4 trillion means that the government added up the values of ALL of its assets. Every tank. Every aircraft carrier. Every acre of land. Every penny in the bank.

And then subtracted its enormous liabilities, like the national debt.

The difference is negative $20.4 trillion, i.e. the government has far MORE liabilities than it has assets.

If the government were a business, it would have gone bankrupt long, long ago.

On top of that, though, the government separately calculated its long-term liabilities from Social Security and Medicare. The number here is negative, too. Minus $49 trillion, to be exact.

Altogether, the government is in the red by almost $70 trillion.

And to make this absolutely clear: These are not vague estimates by a stranger in some dark corner of the internet.

I got these numbers straight from the US Treasury’s 2017 financial report that you can download here.

Inside you can verify yourself that what is written on this page are facts signed by US Treasury Secretary Steven Mnuchin.

According to the government’s own projections, trillion-dollar budget deficits are on the horizon for the next decade. And to run any budget deficits, the US government must auction off new debt.

This is going to be incredibly difficult.

Uncle Sam’s most reliable foreign lenders over the past decade (China and Japan) have decreased their US Treasury holdings.

And last, starting in September 2017, the Federal Reserve started a new “quantitative tightening” program.

That’s fancy lingo to say that as its Treasury bond holdings expire, the Fed won’t rapidly reinvest in new bond purchases. This new policy is the opposite of what the Fed has done over the past decade – buy massive amounts of government debt.

With fewer buyers for US government bonds, the interest rates on those new bonds will be higher. It’s basic supply and demand.

Bottom line, all these trends lead to higher interest rates… at a time when the US government will need to borrow even more money to finance its annual budget shortfalls.

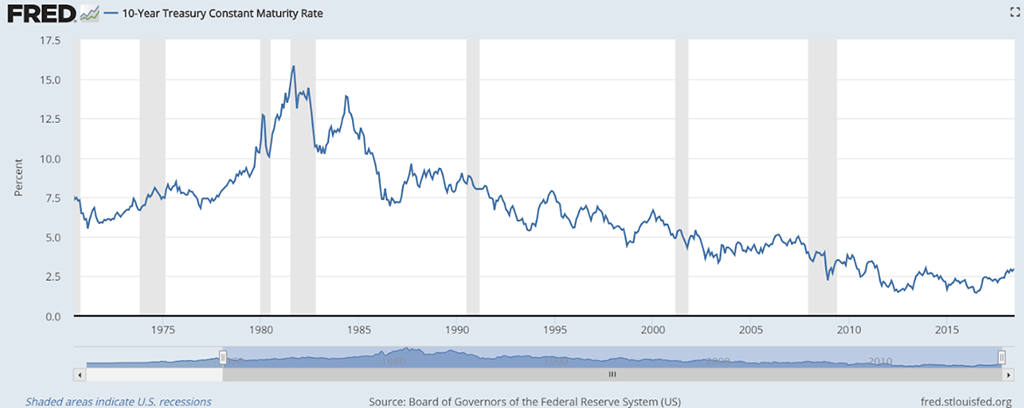

Imagine if the 10-Year Treasury rate returns to its early 1980s rate of over 15%. (The current 10-Year Treasury yield is just under 3%.)

But the 10-Year yield wouldn’t need to climb anywhere near 15% to create chaos. Since 1980, the average rate on the 10-Year is 6.25% – more than double the current rate.

Rising interest rates mean that the US finances would quickly resemble Japan’s debt situation: the percentage of tax revenue spent just on the interest for newly-issued government debt would skyrocket.

The growing rate of interest rate payments is probably the government’s most alarming economic indicator – because the more quickly the government’s interest payments grow, the more money they have to borrow just to pay interest on the money they’ve already borrowed.

The government enters this borrowing-interest rate death spiral. And it’s not pretty.

“We owe the debt to ourselves” is often the government debt apologist’s position.

Sure, the US government owes a sizable portion of the national debt to its own agencies and trust funds.

But, if borrowing from the future to finance the present was the magical answer, why would government tax its citizens? Shouldn’t borrowing suffice to fund government operations?

And is there a fundamental difference between a private person or a private company’s debts and the government’s debts?

Consider what happens to an individual who has racked up too much debt. Imagine if he tried to issue an IOU to his friends, family and coworkers. No sane person would exchange their money for his worthless IOU.

In fact, the debtor may face a freeze on his credit. A court order may force wage garnishments, so his paycheck shrinks considerably. In the dead of night, a repo team may seize his car. He may be forced to liquidate his prized possessions… even his house.

Too much debt ultimately lands a government in the same place as any indebted individual. Because borrowed money must eventually be paid back – regardless of private or public debt.

Still, the insolvent federal government somehow gets a pass.

When the government regularly issues its IOUs (Treasury bonds), other governments, central banks and individuals will circle the block for a chance to exchange their money.

The only thing that’s different between the individual debtor and the federal government debtor is that people’s perceptions and feelings have magically changed. The individual debtor cannot capture his creditor’s full faith and confidence. But, the spendthrift politicians, power and mystique of the US federal government sure can.

But I fail to see how it’s comforting to Social Security beneficiaries that their government must borrow money just to pay interest on the money owed to them.

With a little loss of confidence in the government, the whole equation changes. Once-dependable creditors who suddenly refuse to buy more debt could start a frenzy. And a default would definitely erode individuals’ full faith and confidence in the US government.

Since the US federal government continues down this debt binge highway, someday its credibility will vanish.

In this section you’ll learn why the unfortunate and short answer is… No.

In fact, it’s MATHEMATICALLY impossible for the US to pay off the national debt…

I’ve worked out a financial model which shows that, even with absurd assumptions (7%+ GDP growth for years at a time, low interest rates, etc.), it is simply not feasible for the US government to ‘grow’ its way out of the debt.

You can watch a video where I walk you through this model here…

Even if the government takes on no additional debt, the overall debt level has grown so large that it will still climb.

Yes, you read that right.

Let me explain…

Government expenses are divided into three broad categories:

1. Discretionary Spending

This is what Congress debates about endlessly—deciding how much money each department of government will receive every fiscal year.

2. Mandatory Spending

These are programs like Social Security, Medicare, etc. which are set by law.

Congress doesn’t have to debate anything with these programs. The money just automatically gets sucked out of the Treasury, just like your monthly mortgage payment.

3. Interest on the debt

Last is interest on the debt, which, sadly, is so big that it has its own category.

Why It’s MATHEMATICALLY impossible for the US Govt to pay off the national debt

Right now the system is so screwed up that if you add up the mandatory spending programs AND interest on the debt, the total is nearly as big as ALL of the government’s tax revenue.

In other words, the government could COMPLETELY CUT FUNDING for these 14 departments:

… And the government’s annual budget would still be in the red.

And I want to stress once again that this claim is not based on vague assumptions that I have made. It’s straight from the latest financial statement the Treasury Department has released.

In Fiscal Year (FY) 2017, the government collected $3 trillion in total tax revenue.

But the government also spent $2.15 trillion on Social Security and Medicare and $720 billion on Defense.

And in FY 2017, interest payments on the debt hit a new high of $458 billion – about 15% of its tax revenue… just to pay interest.

So – just between interest, Social Security, Medicare and defense, the government spent $3.3 trillion.

And the budget projections don’t look any better.

In Fiscal Year 2019, the government projects that spending will be nearly $4.4 trillion.

And the US government projects to collect $3.4 trillion in taxes – leaving a gaping $1 trillion hole in the government’s annual finances.

And increasing taxes will not help the US pay off its debt either...

If the government cannot resolve the debt by spending cuts, maybe there’s hope in the other side of the equation – increasing taxes. But you soon discover that this too is a fruitless endeavor.

According to government data, since World War II, America’s overall tax revenue as a percentage of Gross Domestic Product has averaged 17.2%.

The top marginal tax rate has been as low as 28% in the 1980s and as high as 94% right at the end of WWII.

Meanwhile, over the course of US history, the top corporate tax rate has been as low as 1% and as high as 53%.

And yet in all this time, despite enormous variations in tax rates, overall tax revenue as a percentage of GDP has barely budged.

Again, none of this information is Simon Black’s biased opinion or quackery sourced from some demented conspiracy theorist’s website.

Instead, this is real data, straight from government sources and available for public viewing.

If one dates to peek under the curtain, the debt problems are readily apparent.

We’ll next cover how this affects you.

How do you like this article?

Click one of the stars to add your vote...

Other readers gave this article an average rating of 4.9 stars.

The US national debt is not just a problem for the US Government, it's even more of a problem for YOU and you'll learn why in this section.

Let’s summarize: The US government is painted into a nasty debt corner.

We’ve discovered that cutting all discretionary spending outside of defense (a spending plan would never make it through any Congress) still wouldn’t solve the debt problem.

And neither will tax increases, as people and businesses would just move overseas to greener pastures.

The problems keep mounting.

But none of the Congressional Budget Office’s projections really take into consideration anything major. Their forecasts are all based on business as usual – no major financial crises, no major wars and continued, low interest rates.

On the slight chance that 2017 becomes the blueprint for the future (i.e. nothing bad happens), at some point the math still doesn’t work.

The default risk is out there. It’s just that not many are talking about it… or believe that it can happen to the US.

What could that mean? The US government has three options:

1. Default on its foreign creditors (especially foreign governments).

The only reason the US government has been able to borrow this much money is because the US dollar is the reserve currency of the world and everyone believes in the US government’s ability to pay back any debt.

But if the government defaults on one of their creditors, this trust will disappear and nobody will want to lend money to the US. At least not at interest rates the government could afford to pay.

This would cause a global financial and banking crisis the world has never seen.

2. Default on the Federal Reserve, which owns trillions of dollars of US debt.

But this would create an enormous crisis for the US dollar… which would cause chaos for dollar holders. (More on this below.)

3. Default on its obligations to its citizens.

Hopelessly indebted Governments are well aware of the negative consequences of option 1, 2. That’s why this is the most likely option they will choose.

They’ll do this in two ways.

They’ll do this in two ways.

1. A Social Security And Medicare Default

First they’ll default on their obligation to provide retirement income from the Social Security program that people have spent their entire lives paying into.

This is something you can absolutely count on.

Every year the respective Boards of Trustees for Medicare and Social Security release their annual reports where they project when these funds will be depleted.

In the case of Medicare, the Trustees project that its largest trust fund will be fully depleted in 2026, just eight years away. The Social Security Trust Care fund has a similar fate and is projected to be fully depleted in 2034.

In the context of retirement, that’s right around the corner.

And I want to stress once again that this claim is not based on vague assumptions that I have made. It’s straight from the annual reports of Social Security and Medicare.

2. A Default On the US Dollar

Second, they will they’ll default on their obligation to maintain a sound and stable currency through inflation.

Throughout history, inflation has been the option of choice for hopelessly indebted governments.

Since the US dollar is nothing but an empty promise of the US government, they can simply create more dollars out of thin air… thereby devaluing every other dollar in circulation.

This allows them to pay back their creditors with dollars that are worth ‘less’… until the US dollar literally becomes worthless and everyone who holds it loses their purchasing power.

None of these is a good option. And simply put, the US government has reached a point of no return.

No matter how they solve the problem, you’ll, frankly, be screwed… unless you take steps NOW to hedge against the damage.

No-Brainer Strategies to Ensure You Thrive No Matter What Happens Next

Learn about these and many more strategies in our free Perfect Plan B Guide.

They will ensure you are in a position of strength and won’t just survive the inevitable consequences of the US national debt, but will actually benefit and thrive from them.

When faced with these options, it’s clear that one of the paths of least resistance is to forfeit the financial obligations promised to its citizens.

About 10,000 Americans each day turn 65. This trend will continue for years, as more individuals in the massive Baby Boomer generation join the ranks of Social Security and Medicare-eligible recipients.

But, while more people become eligible for these programs, the funding won’t be there for them.

And Social Security will continue running larger and larger deficits until it’s depleted in 2034.

In the context of retirement, those dates are right around the corner.

These numbers come directly from the Trustees of Social Security and Medicare.

And while the sobering reports got mainstream press coverage in 2018, the analysis largely missed the mark. Some newspapers tried to play down the news, telling their readers that Social Security and Medicare are just fine, and that those projections don’t matter.

They’ll state, for example, that there’s nothing to worry about because the government will step in and bail out the programs.

But who will bail out the government?

We’ve already covered how Uncle Sam is insolvent to the tune of $20.4 trillion.

The government needs to course correct this financially impossible situation. And the government’s path of least resistance is to ignore the promises made to its citizens.

Those who are receiving Social Security and Medicare payments – or hope to receive these benefits soon – can expect a substantial cut (i.e. 25% or more) in the benefits that they worked their entire lives to achieve.

The US government can also concoct a new retirement scheme that substantially raises the Social Security age requirement. In fact, other governments have already done this.

For example, in mid-June 2018, the Russian government announced that starting in 2028, the state pension age for men would rise from age 60 to 65. The World Bank’s life expectancy for Russian men is 66… which is very convenient for the Russian government’s precarious pension system.

Now is the time to take charge of your retirement finances. Now is the time to prepare for when the government inevitably defaults on you.

The ones who’ll face significant financial hardships because of the government’s enormous debt are not just future generations or future Social Security recipients counting on this money.

Price inflation is ahead of us. And in every inflationary cycle, people lacking assets (i.e. the middle class and young people) get hosed.

If you’re a rich person who makes $1 million per year and only spends $50,000 per year on living expenses, you’ve got $950,000 remaining to invest. And if all prices rise by 10%, you’ve just made $95,000 per year on your stocks. Meanwhile, your living expenses only went up by $5,000. So, inflation makes you net positive $90,000 richer.

Now, let’s think about the average person making $50,000 per year… with $50,000 of yearly expenses. He faces the same 10% yearly price inflation as the rich guy. But, now with annual expenses of $55,000 and no increase in his earnings, the average person now has $5,000 less than he needs each year. And he’ll have some hard decisions to make.

And the pain for average guys doesn’t just stop during inflationary cycles.

When inflation continues, a downward spiral to stagflation – rising prices and a contracting economy – often follows. The economy suffers under the weight of higher prices and wages may not rise commensurately. Some people ultimately lose their jobs.

Predictably, politicians enter the picture and make the situation worse.

In an economic crisis, politicians have the cover to freely admit that it’s imperative for them to now tax and spend more. Then in the background, often unnoticed, new currency creation goes into hyperdrive, resulting in even worse price inflation. And runaway price inflation further hurts the already injured average citizen.

In western civilization – especially the US – there’s this view that the government can continue incur debts indefinitely and without consequence.

And the individuals who’ll pay for this financial profligacy will not be the current generation, but future generations… even unborn generations decades from now.

Soon, the US won’t be able to pretend that its finances are sustainable. It simply won’t have the means to safeguard the wealth of future generations.

Even if your children and children’s children are lucky enough to be born when the country hasn’t yet defaulted, they’ll spend most of their working lives – if they can even find a job – paying off debt that they had nothing to do with.

This means higher taxes, an increase in civil asset forfeitures, no retirement options and overall, diminished opportunity.

If you’re in the US and all your savings and/or assets are in that fragile, bankrupt US basket, you’re in trouble.

It sounds fear-driven and paranoid. But, this is about facts and numbers. And the numbers don’t lie.

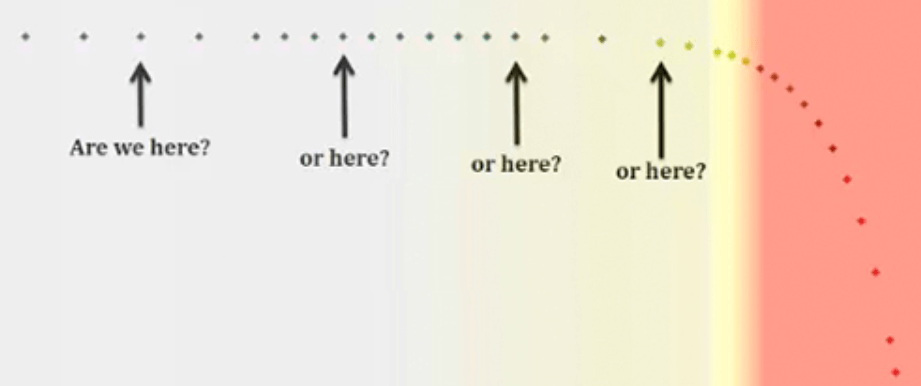

“Gradually and then suddenly” is how a character from Ernest Hemingway’s The Sun Also Rises describes the path to personal bankruptcy.

Nations go bankrupt in the same way. Banking collapses occur in the same way. Currency crises strike in the same way. They all happen gradually… and then suddenly.

We don’t know where we are in the collapse cycle.

The truth is, no one knows exactly where we are right now.

We don’t know whether we’re 6 months or 6 years away from a big reset.

However, we do know a big reset is on the way, because this is not a consequence-free environment. People in other enormously indebted countries have discovered that there are consequences to reckless government finances.

How do you like this article?

Click one of the stars to add your vote...

Other readers gave this article an average rating of 4.9 stars.

In this final section you’ll a few simple steps you can take today to protect yourself and benefit from the consequences of the US national debt.

The United States is not the first super-power that has reached its peak and started its inevitable decline and we can learn from history about how to deal with this situation.

In Rome, for example, all along the way down there were the people who figured, “This has GOT to be the bottom. It can only get better from here”.

Their patriotism was rewarded with reduced civil liberties, higher taxes, insane despots and a polluted currency.

The other group consisted of people who looked at the warning signs and thought, “I have to save myself”. They followed their instincts took steps to build their lives, survive, and prosper.

And that’s what we’ll talk about now:

I see three options.

1. Ignore the debt altogether

If you’re reading this article, you’ve already progressed past this stage.

2. Recognize the problems… but do nothing

Still, others recognize the massive debt problems, but keep their feet planted. They do nothing. They may figure that even at $21 trillion of debt and counting, everything seems fine.

So, if things go south, they’ll just await some government white knight – the very one who caused the debt fiasco – to swoop in with check in hand and save the day.

Sure, there are times when doing nothing is an effective strategy – like passing on that overvalued stock that your coworker recommends. Or, choosing to NOT invest in a seemingly lucrative real estate deal because the developer isn’t a trusted counterparty.

But when facing a government default, doing nothing is your worst enemy.

When countries, central banks and commercial banks accumulate too much debt, and specifically too much debt relative to assets, you can be certain there is trouble ahead in the system.

And the all-too-familiar government blueprint is to grab and/or debase their citizens’ money, and impose draconian capital controls so no one can withdraw remaining funds.

So, if you’re doing nothing, you’re susceptible to this cockamamie scheme that government leaders are nearly guaranteed to cook up in the next crisis.

Fortunately, there’s a solution behind door number three where you’ll be prepared.

3. Take action

This is the door for rational individuals who realize there might possibly be some consequence from the largest debt pile that has ever been accumulated in the history of the world… and they make sensible preparations just in case.

Want to see what’s behind door number three? Read on.

Get The Most ACTIONABLE Info Right Away...

The national debt is not the only problem in the system you are up against… We’ve created a quick-start guide on how to build your personal Plan B.

A Plan B is a set of simple strategies you implement to ensure you thrive no matter what happens next in the world.

Download our Perfect Plan B Guide and learn…

No-Brainer Strategies to Ensure You Thrive No Matter What Happens Next

Learn about these and many more strategies in our free Perfect Plan B Guide.

They will ensure you are in a position of strength and won’t just survive the inevitable consequences of the US national debt, but will actually benefit and thrive from them.

In preparation for the consequences from the rising US debt – a government default and/or significant price inflation – it makes all the sense in the world to take some common-sense precautions to protect yourself.

We know there are risks out on any road, so we simply buckle our seat belt for a degree of protection. Even if you make it from point A to point B unharmed, you’re never worse off for taking a few seconds to secure your seat belt.

Likewise, there are no downsides to these solutions. If the US government manages to continue kick the can down the road successfully for years to come and you don’t end up feeling any pain, you won’t regret taking some precautions.

Because all of these steps are designed to make sense no matter what happens next– even if nothing happens at all, you’ll still be better off.

Some of these solutions require minimal travel and effort… and in some cases (opening an offshore bank account), you don’t have to leave the comfort of your home.

Step #1: Move a portion of your savings to a strong, stable bank outside of the US

The first solution is to move a portion of your savings from the US financial system overseas to a more stable jurisdiction. A place like Hong Kong or the country of Georgia certainly fits the bill.

Just like the US government, US banks are in a precarious position and may not be able to weather another financial shock.

Offshore banks are more conservative – with higher liquidity and solvency ratios – than US banks. These banks are largely not invested in toxic derivatives… the kind of financial insanity that brought down the US banking system back in 2008.

This will protect you from a potential banking crisis and ensure you always have access to emergency funds.

You may also want to consider keeping a portion of your savings in another currency to protect yourself from the decline of the US dollar. The Hong Kong dollar is the perfect currency for this…

Since 1983, the Hong Kong dollar (HKD) has been “pegged” to the US dollar at 7.8, +/- a very narrow range.

This means that, for US dollar investors, you could deposit US dollars at a bank in Hong Kong, and then convert those US dollars into Hong Kong dollars (and back) at minimal cost.

Holding Hong Kong dollars makes a lot of sense.

If the US dollar goes through a period of strength, the Hong Kong dollar will mirror that strength.

But if there’s ever a major loss of confidence in the US economy and the US dollar starts to depreciate rapidly, the Hong Kong Monetary Authority (country’s central bank) could simply “de-peg” and let the Hong Kong dollar appreciate versus US dollar — thereby preserving the purchasing power of your savings.

So, holding Hong Kong dollars gives you ALL of the benefits of holding US dollars, but with free downside protection in the event of any major US financial catastrophe.

Although you can hold your savings in the Hong Kong dollar in many banks around the world, we recommend you open an account in Hong Kong itself – USD-to-HKD currency conversion fees are minimal there.

You can download our Ultimate Offshore Banking Guide to everything you need to open an ultra-safe Offshore Bank Account.

Inside you’ll learn:

You can learn more in our in-depth article about offshore banking here.

Step #2: Purchase precious metals and store them abroad

You can remove some anxiety about the US dollar’s viability by taking another portion of your savings and converting it a 5,000 year-old, proven store of value: gold.

Gold is a conscious decision to park your savings in something besides constantly depreciating fiat (government) money.

Gold is a liquid form of savings, too. But, I’m not holding gold to one day exchange it for more fiat currency down the road (although you can walk into any coin shop around the world and walk out with currency if you need to).

I hold gold to preserve my long-term purchasing power.

You should store some gold at home in your safe. But for large holdings, you should consider diversifying internationally in stable, safe jurisdictions.

Secure overseas precious metals storage in Europe and Asia is available.

One such precious metals storage company in Singapore even allows its depositors to borrow against their holdings – giving the customer liquidity and providing a lender a collateral-backed loan at a market interest rate.

Step #3: Invest internationally

Have you ever filled out those questionnaires that ask you about risk tolerance?

The likely options are “low risk and low returns.” Or “high risk and high returns.”

Sadly, these questionnaires never feature an option for “none of the above.”

Fortunately in the real world, you’ve got a third option – one that blends low risk with high returns.

But, you need to know where to look.

The steeply overvalued US stock markets cannot offer this optimal blend of low-risk, high-return. The same goes for the US bond market. US real estate doesn’t fit the bill, either. And nearly every other asset class in America is priced too high.

The solution: Look overseas.

Wait… foreign markets have a degree of risk, too, you might contend.

I don’t deny that. But nothing in this world is risk-free. Keeping a balance in your checking account isn’t risk-free. Stashing cash under your mattress isn’t risk-free. Doing absolutely nothing with your money isn’t risk-free.

Think in terms of risk-adjusted return. Do you want to be fully invested in all-time high US stock market or stable, foreign stocks that are trading for less than the company has in cash?

That’s right. Deep value investing is like buying $1.00 of value for $0.50 in price.

My team scours thousands of foreign stocks to find amazing opportunities like this. And our track record is phenomenal: At the time of publishing 96% of our stock picks over the past couple of years have been winners, returning investors an average of 44%.

Visit our resources page to find out more about investing outside the mainstream, including internationally.

Step #4: Become a resident of another country and consider getting a Second Passport

Also, another risk mitigation tool – an insurance policy, if you will – is a permanent residency overseas.

A permanent residency guarantees that no matter how bad things get in your home country, you’ll have a welcoming place to live, travel, work and conduct business. And with a permanent residency, your children will have more global opportunities, too.

And you won’t regret getting a second passport that may expand your visa-free international travel options. Plus, the gift of a second citizenships can benefit many future generations.

Some jurisdictions only require minimal time on the ground to secure citizenship. Giving birth in some countries grants you expedited citizenship.

You can even review your family tree. If you have an Italian, Irish, Polish or Lithuanian ancestor, for example, you may be eligible for a second citizenship and passport.

Click over to our free page on second passports and discover how you can get started.

Learn More No-Brainer Strategies To…

Ensure You Thrive No Matter What Happens Next

The above steps are just an introduction to the options available to you.

Download our Perfect Plan B Guide and learn how to…

No-Brainer Strategies to Ensure You Thrive No Matter What Happens Next

Learn about these and many more strategies in our free Perfect Plan B Guide.

They will ensure you are in a position of strength and won’t just survive the inevitable consequences of the US national debt, but will actually benefit and thrive from them.

The world is not coming to an end. America isn’t going away.

That’s not the case.

In fact, I’m optimistic about the tremendous opportunities that the future holds.

Periods of economic expansion are always followed by downturns. Booms are always followed by busts. Powerful nations throughout history who have gotten themselves too deeply into debt always decline.

I’m not talking about anything new here. These trends are thousands of years old.

I’m simply highlighting some obvious data – data which is published by the US government itself – and suggesting that it makes sense to understand these trends, and prepare for some of the possible outcomes.

If financial markets have been expanding for a decade and are selling for record high valuations, it might make sense to consider taking some money off the table.

If all of your income, savings and livelihood happen to be located in a country whose government is completely insolvent and growing worse by the year, it might make sense to consider spreading your assets around the world to safer, more reliable jurisdictions.

I encourage you to take advantage of these obtainable, international solutions. They require neither large commitments of time, nor money.

Think about which combination is right for you and your family.

The time to put your seat belt on is now – while you can and when you’re thinking clearly.

By reading this article and pondering the world’s problems, you’re already on the right track and well ahead of your peers.

At Sovereign Man, we have several thousand premium subscribers and well over 100,000 free Notes from the Field subscribers. Our subscribers are reading our intelligence reports and taking action to better their lives.

But, this community is a tiny fraction of the world’s population.

Imagine if hundreds of thousands or millions of people suddenly realize the precarious financial condition of many western countries. And then this horde of people try to establish foreign residency or move their funds to a well-capitalized overseas bank.

Do you want to be caught up in this crowd and have the door potentially shut on you?

Or, do you want to be well ahead of the curve and ensure that you, your family and your wealth is protected?

The only way to guarantee that you’re in the latter group is to take action.

How do you like this article?

Click one of the stars to add your vote...

Other readers gave this article an average rating of 4.9 stars.